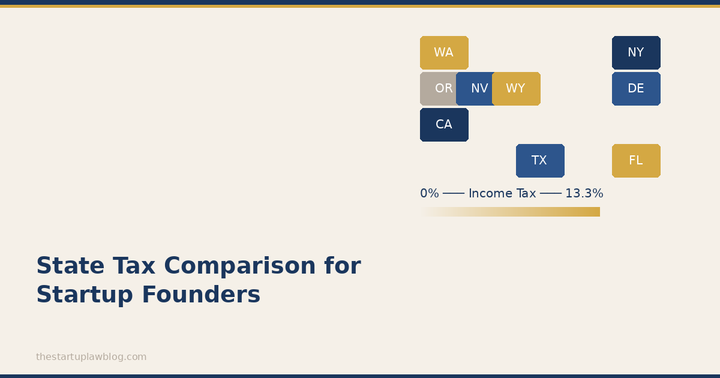

Washington’s 9.9% Income Tax: The Marriage Penalty in ESSB 6346 (and How to Plan)

Washington’s 9.9% income tax (ESSB 6346) uses a $1 million threshold per household, not per person. That creates a marriage penalty: two unmarried high earners can avoid tax while a married couple pays a five-figure bill. Here’s the math—and planning ideas.