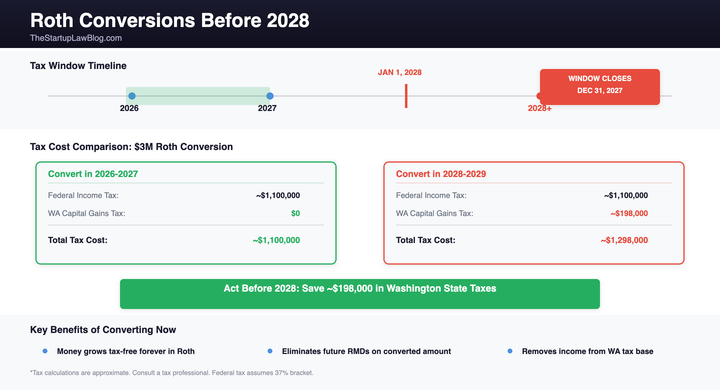

If you are a high-income Washington resident with a large traditional IRA or 401(k), you have until December 31, 2027 to do a Roth conversion at zero Washington income tax. Here's why that matters.

This post is part of our Complete Guide to Washington's New Income Tax.

The Setup

A Roth conversion moves money from a traditional IRA (or other pre-tax retirement account) into a Roth IRA. You pay income tax on the converted amount in the year of conversion. In return, the money grows tax-free in the Roth and is generally not subject to income tax on qualified distributions — not on growth, not on qualified withdrawals. Note that the Roth IRA value may still be included in your taxable estate for estate tax purposes.

The conversion amount is included in your federal adjusted gross income (AGI) in the year of conversion.

Until January 1, 2028, Washington has no income tax on this type of income. (The existing capital gains tax does not apply to Roth conversions, as they generate ordinary income, not long-term capital gains.) That means a Roth conversion done in 2026 or 2027 incurs federal tax only — no Washington tax.

Beginning January 1, 2028, Washington imposes a 9.9% tax on Washington taxable income, which is computed from federal adjusted gross income with statutory modifications and then reduced by the Washington standard deduction of $1,000,000. A large Roth conversion that pushes your Washington taxable income above that threshold is expected to trigger the tax under the current statutory structure (assuming the tax survives its pending constitutional challenge and no material legislative changes are enacted before 2028). That changes the math considerably.

For someone converting a larger amount — say $5 million — the Washington tax savings from acting before 2028 can exceed $300,000.

Who Should Be Thinking About This

This strategy is most relevant for Washington residents who have large traditional IRA, 401(k), or other pre-tax retirement account balances (typically $1 million or more), expect their Washington taxable income to exceed the $1,000,000 standard deduction in retirement or when taking required minimum distributions (RMDs), have the cash to pay the federal tax on the conversion without raiding the retirement account itself, and plan to remain Washington residents (or at least won't be moving to a zero-income-tax state before distributions begin).

It is also worth considering for people who are currently in a temporarily low-income year. If you are between jobs, had a business downturn, or are in a sabbatical year where your other income is low, that is an ideal time to convert — you fill up lower federal brackets while Washington's tax is still at zero.

The Backdoor and Mega Backdoor Angles

Backdoor Roth contributions. High earners who are above the income limits for direct Roth IRA contributions often use the "backdoor" strategy: contribute to a traditional IRA (non-deductible), then immediately convert to a Roth. This remains available and is unaffected by Washington's income tax — the conversion of a non-deductible contribution generates little to no taxable income (since you already paid tax on the contribution).

Mega backdoor Roth. If your employer's 401(k) plan allows after-tax contributions and in-service Roth conversions, you can potentially convert up to $72,000 per year (the 2026 IRS defined-contribution limit, including all contributions; higher totals are possible with catch-up contributions) into a Roth. Again, the conversion of after-tax money generates minimal additional taxable income. This strategy works the same before and after 2028 — but if the conversion generates any taxable income (from investment gains in the after-tax account), doing it before 2028 avoids Washington's tax on that income.

The Pro-Rata Rule

If you have both pre-tax and after-tax (non-deductible) money in traditional IRAs, the pro-rata rule applies to conversions. You cannot cherry-pick only the after-tax dollars to convert. The taxable portion of your conversion is based on the ratio of pre-tax to after-tax money across all of your traditional IRAs.

This is a federal rule, not a Washington rule — but it matters because it determines how much of your conversion hits your federal AGI, which is the base for Washington's tax.

If the pro-rata rule is an issue, consider rolling pre-tax IRA money into your employer's 401(k) (if the plan accepts incoming rollovers) before doing a backdoor Roth conversion. This isolates the after-tax money and eliminates the pro-rata problem.

Required Minimum Distributions: The Long-Term Play

Starting at age 73 (75 for those born in 1960 or later), you must take required minimum distributions (RMDs) from traditional retirement accounts. RMDs are included in federal AGI and may be subject to Washington's 9.9% tax if your Washington taxable income exceeds the $1,000,000 standard deduction.

For someone with a $5 million traditional IRA at age 73, RMDs start around $190,000 per year and grow as a percentage of the balance. Combined with Social Security, pension income, and other sources, it is easy for a high-net-worth retiree to cross the $1 million threshold.

Converting to a Roth before 2028 — while Washington has no income tax — eliminates future RMDs on the converted amount and removes that income from Washington's tax base permanently. The long-term compounding benefit of tax-free growth in the Roth, combined with the permanent elimination of Washington income tax on distributions, makes this one of the most powerful planning strategies available in the pre-2028 window.

Roth IRAs have no RMDs during the owner's lifetime. Under current law, most non-spouse beneficiaries who inherit a Roth IRA must withdraw the funds within 10 years (with exceptions for certain eligible designated beneficiaries). Qualified distributions are generally income-tax-free, though earnings may be taxable if the Roth has not satisfied the 5-year holding rule.

Risks and Considerations

You need cash to pay the tax. Converting a large amount generates a large federal tax bill. Ideally, you pay that tax from non-retirement assets. If you withdraw money from the IRA itself to pay the tax, you lose the benefit of tax-free growth on that amount.

You can't undo it. Before 2018, you could "recharacterize" (undo) a Roth conversion if the account value dropped. That option was eliminated by the Tax Cuts and Jobs Act. A conversion done today is permanent.

Federal rates could change. The current top federal rate of 37% is set under the TCJA as extended by the One Big Beautiful Bill Act. If future legislation raises federal rates, converting now at 37% locks in the current rate. If rates drop, you may have been better off waiting. This is inherently a bet on future tax policy.

Washington's tax could be struck down. The income tax faces a constitutional challenge. If the court strikes it down, the urgency of pre-2028 conversions disappears. But planning based on the assumption that the tax will be struck down is risky — the safer approach is to act as if the tax will survive.

The $1 million threshold could change. The legislature could raise or lower the threshold in future years. But the threshold only matters for post-2028 conversions — conversions done before 2028 are tax-free at the Washington level regardless.

What to Do Now

If you are a Washington resident with significant pre-tax retirement assets, talk to your financial advisor and CPA about a Roth conversion strategy for 2026 and 2027. The three questions worth modeling: How much can you convert without pushing into an uncomfortably high federal bracket? Do you have non-retirement cash to pay the federal tax? And what is the projected Washington tax savings from converting before 2028 versus waiting?

If Washington's income tax takes effect as enacted, the window closes on December 31, 2027. Once in effect, every dollar you convert above the Washington standard deduction costs an additional 9.9 cents in state tax. That cost compounds over time — because those are dollars that would otherwise grow tax-free in a Roth for decades.

For more on retirement income and Washington's tax, see Is Retirement Income Subject to Washington's 9.9% Income Tax? and our Washington State Taxes guide. If you also have nonqualified deferred compensation, see Deferred Compensation and Washington's 9.9% Income Tax for how to coordinate your distribution schedule with Roth conversion timing.

If you're planning Roth conversions specifically to reduce exposure before 2028, make sure you understand how Washington's residency rules interact with your timeline. Whether the Washington 30-day rule for tax residency applies — and whether you still qualify as a Washington resident — determines whether the conversion is subject to Washington's income tax.

Frequently asked questions

Does the Roth conversion window really close in 2028?

The federal ability to do Roth conversions does not end in 2028 — conversions remain available indefinitely. What closes is Washington's zero-tax treatment. Beginning January 1, 2028, a conversion large enough to push your Washington taxable income above the $1 million standard deduction is expected to be subject to the state's 9.9% income tax. Conversions completed in 2026 and 2027 face federal tax only.

Will Washington tax my Roth conversion?

Not before 2028. From January 1, 2028, a Roth conversion is included in federal AGI, which is the base for Washington's income tax, so a conversion that takes your Washington taxable income above the $1 million deduction is expected to incur the 9.9% tax — unless the tax is struck down in its pending constitutional challenge.

Is there a deadline for 2027 Roth conversions?

Yes. To fall inside the zero-Washington-tax window, the conversion must be completed by December 31, 2027. A conversion counts in the year the funds actually move, so the transaction should be finished well before year-end 2027, not merely initiated.

Can I undo a Roth conversion?

No. The ability to recharacterize (reverse) a Roth conversion was eliminated by the Tax Cuts and Jobs Act in 2018. A conversion done today is permanent, so model the federal tax cost before you convert.

Does a Roth conversion count toward Washington's $1 million threshold?

Yes. The conversion amount is part of federal AGI, which flows into Washington taxable income. For married couples, the $1 million standard deduction is shared regardless of filing status, so a large conversion can consume the deduction quickly.

This post is for informational purposes only and does not constitute legal or tax advice. Consult with a qualified tax professional regarding your specific circumstances.

A note before you book: please share only the names of the parties and a brief, non-confidential description of your issue. Confidential details should wait until we’ve completed a conflicts check and signed a written engagement agreement.

Thinking about converting before 2028?

Joe Wallin is a startup and tax attorney with 25+ years of experience advising founders and high earners. Book a 20-minute call to talk through whether accelerating your Roth conversions makes sense for your situation.

Book a Free 20-Minute Call →Want the full playbook first? The Washington State Tax Planning Guide covers Roth timing, QSBS, and domicile strategy — $49.99.

Related Posts

- Stock Option Exercise Timing: Planning Before Washington's 2028 Income Tax

- Washington vs. California: A Tax Comparison for Founders and Investors

- QSBS Stacking: How to Multiply the $15M Exclusion with Trusts and Family Gifts

- How to Change Your Washington Domicile to Avoid the Income Tax

- Washington's New Income Tax: The Complete Guide

- Washington Capital Gains Tax: The Complete Guide

- The Washington Founder Exit Map

- The ESSB 6346 Marriage Penalty Explained