By Joe Wallin | April 2026 | ~6 min read

Washington's new income tax reaches cryptocurrency and digital asset gains. If you are a Washington resident with significant crypto holdings, this is something you need to understand — because the interaction between federal reporting rules and Washington's $1 million threshold creates both risks and planning opportunities.

This post is part of our Complete Guide to Washington's New Income Tax.

The Basic Rule: Federal AGI Is the Starting Point

Washington's 9.9% income tax starts with your federal adjusted gross income (AGI). The IRS treats cryptocurrency and digital assets as property, not currency. Every disposal — sale, trade, spend, or exchange — is a taxable event that flows into your federal AGI.

That means every type of crypto transaction that generates federal taxable income also generates Washington taxable income:

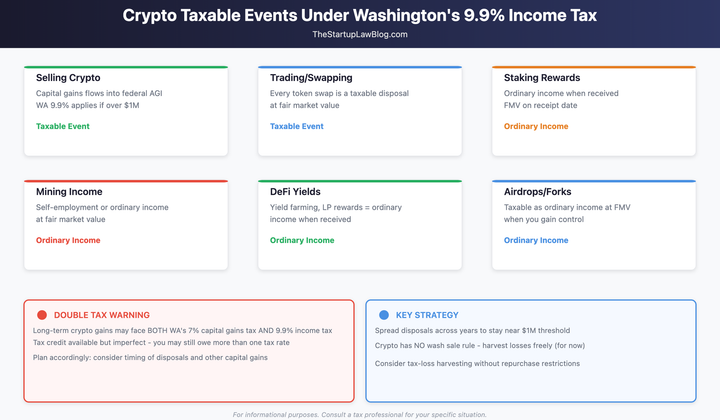

Capital gains from selling or trading crypto. If you sell Bitcoin, Ethereum, or any other digital asset for more than your cost basis, the gain is included in federal AGI. Short-term gains (assets held less than one year) are taxed as ordinary income at federal rates up to 37%. Long-term gains (held more than one year) are taxed at preferential federal rates of 0%, 15%, or 20%. Both are included in federal AGI and are subject to Washington's 9.9% tax if your total AGI exceeds $1 million.

Staking rewards. The IRS treats staking rewards as ordinary income at the time of receipt, valued at fair market value. This income is included in federal AGI in the year you receive the rewards — not when you sell them. If you later sell the staking rewards, any gain above the value at receipt is an additional taxable event.

Mining income. Crypto mining income is treated as self-employment income (if you mine as a business) or ordinary income. It flows into federal AGI.

DeFi yields and liquidity pool rewards. Yield farming income, liquidity provider fees, and other DeFi earnings are taxable as ordinary income when received. Swapping tokens within a DeFi protocol is a taxable disposal of the token you give up.

Airdrops and hard forks. Generally taxable as ordinary income at fair market value when you receive dominion and control over the new tokens.

The common thread: if it hits your federal AGI, Washington taxes it at 9.9% above $1 million.

The Volatility Problem

Crypto's volatility creates a specific problem for Washington's income tax. A single large trade — or a bull market year where you take profits — can spike your AGI well above $1 million, triggering a significant Washington tax bill. The next year, your income might be a fraction of that.

Unlike the federal system, which has graduated rates, Washington's tax is a flat 9.9% on everything above the $1 million line. There is no lower bracket. You are either below the threshold (and owe nothing) or above it (and owe 9.9% on every dollar over $1 million).

This makes timing particularly important. Realizing $3 million in crypto gains in a single year produces a very different Washington tax result than realizing $1 million per year over three years.

The Capital Gains Tax Overlap

Washington also imposes a separate capital gains tax on long-term capital gains: 7% on gains above the standard deduction ($250,000 base, indexed annually; $278,000 for tax year 2025), rising to 9.9% on the taxable portion of gain above $1 million. Crypto gains held for more than one year are subject to this tax as well.

Long-term crypto gains do not generate two separate state-level taxes on the same gain. Under ESSB 6346, long-term capital gains are first stripped out of the Washington income tax base (§302(1)), and the gains subject to Washington's capital gains tax are added back (§302(3)). Section 205 then provides a nonrefundable credit for the capital gains tax paid, capped at the income tax due. Net result: the same long-term gain bears the greater of the two regimes — roughly 9.9% — never both. In practice, long-term crypto gains are taxed under the capital gains tax (7% above the standard deduction, 9.9% above $1 million).

Short-term crypto gains and ordinary crypto income (staking rewards, mining income, DeFi yields, airdrops, hard forks) remain in federal AGI and are subject to the 9.9% income tax above the $1 million threshold. They are not subject to the capital gains tax.

Work with your CPA to model both taxes together.

Planning Strategies for Crypto Holders

Spread disposals across tax years. If you have large unrealized gains, consider selling in tranches rather than all at once. Keeping each year's AGI at or near $1 million — or below it — can dramatically reduce your cumulative Washington tax. This is the same logic as the installment sale strategy, applied to voluntary disposals.

Harvest losses strategically. Crypto losses offset crypto gains for federal purposes, which also reduces your Washington AGI. Unlike stocks, crypto is not currently subject to the wash sale rule under federal law — meaning you can sell at a loss and immediately repurchase the same asset. (Note: Congress has discussed extending wash sale rules to crypto, and the IRS has signaled interest. This could change. Check the current rules before executing.)

Time your staking and DeFi activity. If staking rewards and DeFi yields are pushing your AGI above $1 million, consider the timing of when you activate or deactivate staking positions. Rewards are taxable when received — pausing staking in a high-income year can keep AGI below the threshold.

Use long-term holding periods. While both short-term and long-term gains hit your federal AGI (and thus Washington's tax base), long-term gains are taxed at lower federal rates. Holding crypto for more than one year reduces your total tax burden even though the Washington rate is the same.

Consider the PTE election for crypto held in an entity. If you hold crypto through an S corp, partnership, or LLC, the PTE election can reduce the effective Washington rate from 9.9% to approximately 6.2% (the math is 9.9% × (1 − 37% federal rate), assuming the owner is in the top federal bracket). This applies only to crypto activity that qualifies as pass-through business income — typically fund managers, active trading entities, and mining operations structured as pass-throughs. Passive crypto investing held inside a holding entity generally will not qualify.

Track your basis meticulously. With Form 1099-DA now required from centralized exchanges starting in 2026, the IRS has better visibility into crypto transactions than ever. Accurate basis tracking — including specific identification of lots — allows you to minimize gains by selling highest-basis lots first (specific identification method) or using other permitted accounting methods.

NFTs and Other Digital Assets

NFTs, tokenized real-world assets, and other digital collectibles follow the same general rules. Disposals are taxable events, and gains flow into federal AGI. If the asset is treated as a collectible for federal purposes (which some NFTs may be), the federal capital gains rate can be as high as 28% — and the gain still flows into Washington's tax base.

The classification of specific digital assets is still evolving at the federal level, and Washington's tax simply follows the federal treatment. Stay current with IRS guidance on the classification of your specific assets.

The Reporting Environment Is Tightening

Starting in 2026, centralized exchanges are required to issue Form 1099-DA to both the IRS and the taxpayer, reporting gross proceeds from crypto disposals. This is a significant change from prior years, when reporting was inconsistent and many taxpayers self-reported (or didn't).

Washington's income tax piggybacks on federal AGI, which means accurate federal reporting automatically flows into your Washington obligation. If the IRS adjusts your federal AGI based on 1099-DA reporting, Washington can follow suit.

The era of informal crypto tax reporting is over. Make sure your records are clean, your basis calculations are defensible, and your CPA understands your full transaction history.

Key Takeaways

Long-term crypto gains are taxed under Washington's capital gains tax regime (7% above the standard deduction, 9.9% on taxable gain above $1 million). From 2028 they also enter the income-tax base via ESSB 6346 §302(3), but §205 credits the capital gains tax paid — so the same gain bears one Washington layer, not two. Short-term crypto gains and ordinary crypto income (staking rewards, mining, DeFi yields, airdrops, hard forks) flow into federal AGI and are subject to the 9.9% income tax above $1 million. The flat rate and hard threshold make timing and loss harvesting particularly powerful tools — model both taxes together.

If you are a Washington resident with significant digital asset holdings, start planning now — before January 1, 2028.

For more on Washington's income tax framework, see our Washington State Taxes guide. For a deeper look at loss harvesting techniques (including the crypto-specific advantage of no wash sale rule), see Tax Loss Harvesting to Manage Washington's $1 Million Threshold.

This post is for informational purposes only and does not constitute legal or tax advice. Consult with a qualified tax professional regarding your specific circumstances.

Related Posts

- Equity Compensation Plan Design: How to Structure Your Startup's Stock Option Plan

- ISO vs. NSO: The Complete Guide to Incentive Stock Options and Nonqualified Stock Options

- Founder Vesting Schedules: Why Every Co-Founder Needs One and How to Get It Right

- Stock Option Exercise Timing: Planning Before Washington's 2028 Income Tax

- Washington vs. California: A Tax Comparison for Founders and Investors

- Washington's New Income Tax: The Complete Guide