By Joe Wallin | April 2026 | ~10 min read

The Section 1202 QSBS exclusion can shelter up to $15 million in capital gains from federal tax. But does a married couple get one $15 million exclusion — or two?

This is one of the most common questions I get from founders and investors, and the answer is frustratingly uncertain. The statute doesn't directly address it. The IRS hasn't issued definitive guidance. And the stakes are enormous: the difference between a $15 million exclusion and a $30 million exclusion on a successful exit is, at current rates, roughly $3 million in federal capital gains tax.

This post walks through the statutory text, the arguments on each side, the planning strategies that practitioners are using, and the risks you need to understand before relying on any of them.

01 — The Statutory Framework: What Section 1202 Actually Says

Let's start with the text, because the answer to this question lives — or fails to live — in the statute.

Section 1202(a) provides that a taxpayer may exclude from gross income a percentage of gain from the sale of qualified small business stock (QSBS) held for more than five years (or, after the One Big Beautiful Bill Act, graduated percentages for stock held three, four, or five years).

Section 1202(b)(1) caps the amount of gain eligible for exclusion at the greater of $15 million (as adjusted for inflation starting in 2027, for stock issued after July 4, 2025) or 10 times the taxpayer's adjusted basis in the stock.

Here is the critical provision. Section 1202(b)(3) says:

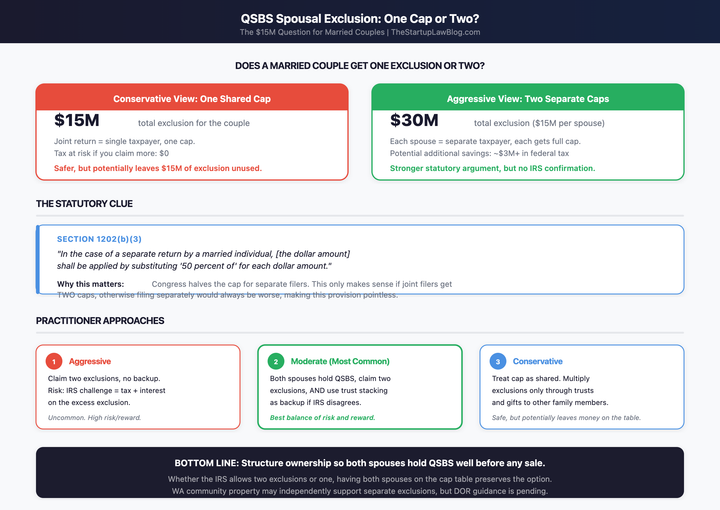

"In the case of a separate return by a married individual, [the dollar amount] shall be applied by substituting '50 percent of' for each dollar amount."

In other words, if you file married filing separately, your cap is halved — $7.5 million instead of $15 million (and $5 million instead of $10 million for pre-OBBBA stock).

And that's it. That is everything Section 1202 says about married couples.

The statute does not say: "In the case of a joint return, the exclusion applies once per couple." It does not say: "In the case of a joint return, each spouse is treated as a separate taxpayer with a separate cap." It simply addresses the married filing separately case and leaves the joint return question unresolved.

This silence is the source of the entire debate.

02 — The Core Question: "Taxpayer" Means What, Exactly?

The exclusion applies to "the taxpayer." The cap is measured against gains recognized by "the taxpayer." The basis computation uses "the taxpayer's" adjusted basis.

On a joint return, is "the taxpayer" the married couple filing together? Or is each spouse a separate "taxpayer" who happens to be filing on the same return?

This is not a new question in tax law. Different Code sections treat joint filers differently. Sometimes Congress intends a single cap per return. Sometimes it intends a cap per person. When Congress wants to be clear, it usually says so — and in Section 1202, it didn't.

03 — The Argument for Two Separate Exclusions

The argument that each spouse gets a separate $15 million exclusion rests on several pillars:

The statute's own structure implies it. Section 1202(b)(3) cuts the exclusion in half for married filing separately. Arguably the most natural reading is that this halving prevents doubling — it ensures that a couple can't file separately and each claim the full amount, effectively getting $30 million instead of $15 million. If the joint return already limited the couple to one shared $15 million exclusion, the married-filing-separately reduction would make no sense. Why halve something that was never doubled?

In other words, the reduction for separate filers only makes logical sense if joint filers get two full exclusions. Otherwise, filing separately would always be worse, and the provision would be pointless. (A competing interpretation — that the halving addresses community property duplication rather than signaling two exclusions — is discussed below, but should be noted here as a credible alternative. It is also worth noting that Congress frequently uses married-filing-separately haircuts as a default penalty rule even where there is no doubling risk — the AMT exemption phaseout and various credit phaseouts follow this pattern — which means the halving in §1202(b)(3) does not necessarily imply that joint filers get two exclusions.)

The term "taxpayer" generally refers to the individual. Section 7701(a)(14) defines "taxpayer" as "any person subject to any internal revenue tax." A married couple filing jointly consists of two taxpayers filing a single return. Filing a joint return doesn't merge two people into one taxpayer — it's an administrative convenience.

IRS treatment in analogous contexts. In other areas where "per taxpayer" caps exist, the IRS has treated spouses as separate taxpayers even on joint returns. For example, under Section 453A (the installment sale interest charge provision), the IRS has ruled that the $5 million threshold applies separately to each spouse, not once per joint return. While Section 453A is not Section 1202, the analogy is illustrative, not determinative — each Code section must be interpreted on its own terms. But the principle is directionally supportive: where Congress uses "taxpayer" without specifying joint-return treatment, the IRS has at times respected the individual-taxpayer reading.

The legislative purpose supports this reading. Section 1202 was designed to encourage investment in small businesses. Treating married co-founders or co-investors as having only a single exclusion between them would penalize marriage — an outcome that Congress generally avoids.

04 — The Argument for One Shared Exclusion

The conservative position — that a married couple filing jointly shares a single $15 million cap — also has support:

The joint return is a single return. When a married couple files jointly, they compute a single taxable income, a single tax liability, and a single set of deductions and credits. Many Code provisions apply per return, not per individual. Absent explicit language treating each spouse separately, the default reading is that the exclusion applies once per return.

Section 1202(b)(3) can be read differently. The married-filing-separately provision could be intended simply to prevent each spouse from claiming the full cap on a separate return when the stock was community property or jointly held. Under this reading, the halving prevents abuse in community property states, where each spouse might claim the full exclusion on their separate return for their half of the same jointly held stock.

No affirmative IRS guidance supports the two-exclusion position. The IRS has not issued a Revenue Ruling, PLR, or any formal guidance confirming that joint filers get two separate Section 1202 exclusions. The absence of guidance is not conclusive either way, but practitioners who take the aggressive position do so without a safety net.

The "majority view" among advisors is cautious. A significant number of tax practitioners take the conservative position that joint filers share one exclusion. When advising clients on a position worth millions of dollars, many prefer the reading that is less likely to invite IRS challenge.

05 — Community Property States: A Different Wrinkle

For couples in community property states — Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin — there's an additional layer of complexity.

In a community property state, income earned during the marriage and property acquired with that income generally belongs equally to both spouses, regardless of whose name is on the title. If a founder acquires QSBS during the marriage using community funds (or if the stock is community property under state law), each spouse owns an undivided one-half interest in the stock.

This raises the question: if each spouse owns half the stock as community property, and each spouse is a separate "taxpayer," does each spouse get a $15 million exclusion on their half of the gain?

The argument is straightforward in principle but untested in practice. The IRS has not ruled on whether community property ownership of QSBS creates two separate exclusions. And the interaction between community property law and Section 1202 is genuinely complex — the core tension is that Section 1202 applies at the federal taxpayer level, while community property law operates at the state ownership level, and the statute does not resolve which frame controls. This is compounded by the practical reality that the stock may have been issued in one spouse's name, on a cap table that lists only one owner, while state law treats it as co-owned.

Washington founders take note: Washington is a community property state. If you incorporated your startup during your marriage and paid for your founder shares with community funds, your spouse may have a community property interest in that stock. This matters for QSBS planning — and it matters even more now that Washington has a 9.9% income tax that piggybacks on federal AGI. Maximizing QSBS exclusions directly reduces both federal and Washington tax exposure.

06 — The Gift-to-Spouse Strategy

One of the most discussed spousal QSBS strategies is simple in concept: before a sale, one spouse gifts QSBS to the other spouse, so that both spouses hold stock and each claims their own exclusion.

How it works under current law:

Under Section 1041, transfers of property between spouses (or incident to divorce) are not taxable events. The recipient spouse takes the donor's adjusted basis and holding period. For Section 1202 purposes, the stock retains its character as QSBS in the hands of the recipient — the "tacking" rules allow the donee spouse to count the donor's holding period.

So in theory: Founder holds $20 million of QSBS. Founder gifts half to spouse. Founder sells $10 million of QSBS and claims $10 million exclusion. Spouse sells $10 million of QSBS and claims $10 million exclusion. Total excluded: $20 million.

The risks:

This strategy assumes that each spouse is treated as a separate taxpayer with a separate exclusion — the very question that is unresolved. If the IRS takes the position that joint filers share one $15 million cap, the gift accomplishes nothing for exclusion purposes. You've just added complexity without benefit.

There is also a meaningful tension between the literal statutory text and its likely purpose. Section 1202(h)(2)(B) provides tacking rules for all gifts without distinction — but the provision was likely designed to prevent loss of QSBS status on gratuitous transfers, not to facilitate exclusion multiplication between spouses on a joint return. The counterargument is that the statute doesn't distinguish between gifts to a spouse and gifts to anyone else; the tacking rules apply equally to all donees, and reading in a spousal limitation would require adding words Congress did not write.

Practical consideration: If you are going to pursue this strategy, the gift should be completed well before a sale is imminent. A last-minute gift of QSBS on the eve of a sale could invite scrutiny — the IRS could invoke the step-transaction doctrine or argue anticipatory assignment of income if the transfer occurs when a sale is effectively locked in. The cleaner the separation in time and the more genuine the donee spouse's ownership (including, ideally, their own decision about when to sell), the stronger the position.

07 — How the One Big Beautiful Bill Act Changes the Math

The One Big Beautiful Bill Act, signed July 4, 2025, made several changes to Section 1202 that affect spousal planning:

The exclusion cap increased to $15 million (from $10 million) for QSBS issued after July 4, 2025. Starting in 2027, this cap adjusts for inflation annually.

The gross asset limit increased to $75 million (from $50 million), meaning more companies qualify to issue QSBS.

A tiered holding period now applies to stock issued after July 4, 2025: 50% exclusion after 3 years, 75% after 4 years, 100% after 5 years. Pre-OBBBA stock retains the prior rules (100% exclusion after 5 years for stock acquired after September 27, 2010).

The married-filing-separately halving was updated to apply to the new amounts — $7.5 million for post-OBBBA stock on a separate return.

What this means for spousal planning: The stakes are higher. If each spouse gets a separate $15 million exclusion on post-OBBBA stock, that is $30 million of excluded gain — potentially saving over $7 million in combined federal and state tax (depending on rates and state treatment). The incentive to resolve this question — or to plan aggressively — has increased proportionally.

It also means the married-filing-separately argument is stronger. Congress explicitly updated Section 1202(b)(3) for the new $15 million amount. If joint filers only got one $15 million cap, the halving to $7.5 million for separate filers would still make no sense — you'd be halving a per-couple cap, giving each spouse less on a separate return than they could get on a joint return. The structural argument for two separate exclusions on a joint return survives the OBBBA amendments intact.

08 — Spousal Planning vs. Trust-Based Stacking

If the goal is to multiply Section 1202 exclusions, the more established strategy is to gift QSBS to non-grantor trusts — each of which is a separate taxpayer with its own $15 million exclusion. This is the "stacking" technique covered in my QSBS Stacking guide.

Trust-based stacking has clearer legal footing than spousal doubling because each non-grantor trust is unambiguously a separate taxpayer under Section 7701. There is no question about whether the trust gets its own exclusion — it does.

The comparison:

Spousal doubling — simpler to execute (a gift between spouses), but legally uncertain. If the IRS rules against it, the entire benefit disappears. No additional entity formation or trust administration required.

Trust stacking — more complex and costly (requires drafting irrevocable non-grantor trusts, transferring stock, potentially paying gift tax or using exemption), but legally more defensible. Each trust is an independent taxpayer. The primary risk is ensuring the trusts are genuinely non-grantor trusts and that the transfers are completed gifts.

The practical takeaway: Where facts support it, do both — but with a clear hierarchy. Trust-based stacking should be the primary strategy, given its stronger legal footing. Spousal doubling works best as an additional layer where the ownership history supports it — original co-investment, or interspousal gifts completed well in advance of any sale — rather than as a last-minute planning move. Don't build your entire plan around spousal doubling if the IRS could take it away with a single ruling — but don't leave potential millions on the table by ignoring it either.

→ See QSBS Stacking: How to Multiply the $15M Exclusion with Trusts and Family Gifts for a deep dive on trust-based strategies.

09 — What Practitioners Are Actually Doing

Having discussed this question with tax practitioners across the country, here is where the practice seems to land:

Most aggressive position: Both spouses each claim a full $15 million exclusion on their joint return, based on the statutory structure argument and the "taxpayer = individual" reading. No protective measures taken beyond filing the return as claimed.

Moderate position: Both spouses hold QSBS (either through original issuance or gift), each claims a separate exclusion, but the couple also implements trust-based stacking as a backup so that even if the spousal position fails, the overall exclusion is preserved through trust entities.

Conservative position: The couple treats the $15 million cap as shared on the joint return, and relies entirely on trust stacking and gifts to children/other family members to multiply exclusions.

Most common approach: The moderate position. Practitioners advise clients to structure ownership so both spouses hold QSBS, claim two exclusions, and simultaneously implement trust-based stacking for any gain above $30 million (or to serve as a fallback if the spousal position is challenged).

The reason the moderate position dominates is practical: the downside of claiming two exclusions on a joint return is that the IRS could disagree. But the cost of being wrong is a tax deficiency (plus interest), not a fraud penalty — you're taking a position with reasonable basis. Most practitioners would characterize the two-exclusion position as likely supported by reasonable basis, though not clearly rising to substantial authority — an important distinction for penalty exposure when the dollars at stake are this large. And the upside is potentially millions in tax savings.

10 — What Would the IRS Likely Argue?

If the IRS were to challenge the two-exclusion position on a joint return, the argument would likely proceed along these lines:

The joint return is the taxable unit. When a married couple files jointly under Section 6013, they compute a single taxable income and a single tax liability. Section 1202(b)(1) caps the exclusion for "the taxpayer," and on a joint return, "the taxpayer" is the couple — not each spouse independently. Absent explicit statutory language providing a per-spouse cap (as Congress has done elsewhere when it intends that result), the default is one exclusion per return.

The MFS halving is a penalty provision, not a doubling signal. Congress routinely reduces benefits for married-filing-separately returns as a disincentive to file separately — the AMT exemption, the child tax credit phaseout, and numerous other provisions follow this pattern. The halving in §1202(b)(3) is consistent with this general approach and does not logically require that joint filers receive two full exclusions.

Interspousal transfers are exclusion-multiplication devices. Where a founder gifts QSBS to a spouse shortly before a sale, the IRS could characterize the transaction as a step transaction or anticipatory assignment of income — arguing that the economic substance is a single sale by a single taxpayer, with the interspousal transfer serving no independent business purpose other than to claim a second exclusion.

Legislative silence is not legislative permission. The absence of explicit guidance on joint-return treatment is not an affirmative grant of two exclusions. Where the statute is ambiguous, the IRS would argue that the narrower reading — one cap per return — is more consistent with the statute's structure, particularly given the significant revenue implications of the broader interpretation.

Practitioners should be prepared for each of these arguments. The strongest response remains the structural one: the MFS halving makes the most sense as an anti-doubling provision, and "taxpayer" has a defined statutory meaning that refers to the individual. But acknowledging the government's likely position strengthens — rather than weakens — the credibility of the analysis.

11 — Key Takeaways and Action Items

The law is genuinely ambiguous. Anyone who tells you with certainty that married couples do or don't get two separate exclusions is overstating their confidence. The statute is silent on joint returns. The IRS has not opined. No court has ruled.

The structural argument for two exclusions is strong. The married-filing-separately halving provision makes the most sense if joint filers get two full exclusions. This is, in my view, the better reading of the statute — but "better" is not "certain."

Community property matters. In Washington and other community property states, the community property nature of the stock may independently support the position that each spouse has a separate interest and a separate exclusion. This needs to be analyzed in light of your specific state's law and how the stock was acquired.

Don't rely solely on spousal doubling. Use trust-based stacking as your primary multiplication strategy. Treat the spousal question as an additional layer of benefit, not the foundation of your plan.

Structure ownership early. Whether through original issuance (both spouses on the cap table) or interspousal gifts, ensure both spouses hold QSBS well before a sale is contemplated. Last-minute transfers invite scrutiny.

Coordinate with your CPA and tax attorney. The interaction between Section 1202, community property law, the OBBBA changes, and state tax treatment (including Washington's 9.9% income tax) makes this a multi-variable problem. The right answer depends on your specific facts.

Watch for IRS guidance. With the OBBBA expanding the exclusion and the stakes rising, the IRS may eventually address this question through regulations, a Revenue Ruling, or an audit campaign. Stay current.

If you have QSBS and want to discuss spousal planning for your specific situation, I'm happy to help. → Book a call

This post is for informational purposes only and does not constitute legal or tax advice. Consult a qualified attorney or tax advisor for advice specific to your situation.

Related Reading:

→ The Complete Guide to QSBS and Section 1202

→ QSBS Stacking: How to Multiply the $15M Exclusion with Trusts and Family Gifts