If you work at a startup and hold incentive stock options, the alternative minimum tax is probably the most misunderstood part of your compensation package. The AMT can create a tax bill on income you haven't actually received — and the consequences can be devastating if you're not prepared.

This guide explains how the AMT works, how it applies to stock options, what changed in 2026 under the One Big Beautiful Bill Act, and — critically — how Washington state's new taxes interact with the AMT to create planning opportunities that don't exist anywhere else.

In 60 seconds:

- AMT can tax the “bargain element” from an ISO exercise even if you haven’t sold the shares.

- NQSOs are generally taxed as ordinary income at exercise (not AMT), but they come with immediate withholding.

- Washington overlay: capital gains tax (7% above $250,000) plus the 2028 income tax (6.5% above $250,000; 9.9% above $1,000,000) means timing and liquidity matter more than ever.

- Planning levers: stagger exercises, manage AMT credit, and plan liquidity for tax payments so you’re not forced into a bad sale.

What Is the Alternative Minimum Tax?

The AMT is a parallel tax system that runs alongside the regular federal income tax. Every year, you effectively calculate your taxes two ways — the regular way and the AMT way — and you pay whichever is higher.

The AMT was originally designed to prevent wealthy taxpayers from using deductions and credits to reduce their tax bills to zero. But because of how it treats stock options, the AMT routinely catches startup employees who aren't wealthy at all — they just happen to be sitting on paper gains they can't sell.

Here's how the AMT calculation works:

- Start with your regular taxable income.

- Add back certain items that are deductible for regular tax but not for AMT (the "AMT adjustments"). For stock option holders, the big one is the ISO spread.

- Subtract the AMT exemption amount.

- Apply the AMT tax rates (26% or 28%).

- If the result is higher than your regular tax, you pay the difference as AMT.

AMT Exemption Amounts and Rates for 2026

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, made permanent the higher AMT exemption amounts that had been temporary under the Tax Cuts and Jobs Act. But it also made the phase-out rules significantly more aggressive starting in 2026.

2026 AMT exemption amounts:

- Single filers: $90,100

- Married filing jointly: $140,200

AMT tax rates:

- 26% on AMT income up to $239,100 (single) / $239,100 (joint)

- 28% on AMT income above that threshold

The new phase-out rules (this is the big change):

Starting in 2026, the AMT exemption phases out at 50 cents per dollar of alternative minimum taxable income (AMTI) above $500,000 (single) or $1,000,000 (joint). Before 2026, the phase-out rate was 25 cents per dollar.

What this means in practice: if you're a single filer and your AMTI hits $680,200, your exemption is completely gone. For joint filers, the exemption disappears at $1,280,400.

During the phase-out range, your effective marginal AMT rate jumps to roughly 42% — the 28% statutory rate plus the 14% bite from losing the exemption at an accelerated rate. This is a meaningful increase from the pre-2026 effective rate in the phase-out zone.

How Stock Options Trigger the AMT

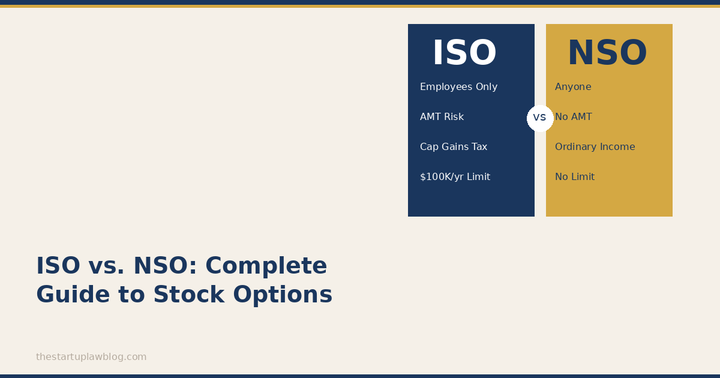

Not all stock options are created equal for AMT purposes. The AMT treatment depends entirely on whether you hold incentive stock options (ISOs) or non-qualified stock options (NSOs).

NSOs: No AMT Issue

When you exercise a non-qualified stock option, the spread (the difference between the fair market value of the stock and your exercise price) is ordinary income. It shows up on your W-2. You pay regular income tax on it. The AMT doesn't care — the spread is already included in your regular taxable income, so there's no AMT adjustment.

ISOs: The AMT Trigger

Incentive stock options are the problem. When you exercise an ISO and hold the shares (rather than selling them immediately), two things happen for tax purposes:

For regular tax: Nothing. You don't recognize any income at exercise. The idea is that you'll get long-term capital gains treatment when you eventually sell — as long as you meet the ISO holding periods (more than two years from grant date and more than one year from exercise date).

For AMT: The entire spread at exercise is treated as AMT income. This is the "AMT adjustment" — the spread gets added to your income for purposes of the AMT calculation, even though it's invisible to the regular tax system.

This creates the classic ISO trap: you owe tax on a gain you haven't realized in cash. If the stock is at a private company, you can't even sell it to pay the tax.

A Worked Example

Let's say you're a single filer in Washington earning $250,000 in base salary. You exercise ISOs with a spread of $500,000 (you exercise 50,000 shares at $2 when the fair market value is $12).

Regular tax calculation: Taxable income: $250,000. Federal tax: approximately $51,600 (2026 rates).

AMT calculation: Start with $250,000 in regular income. Add the $500,000 ISO spread. Your AMTI is $750,000.

Exemption: $90,100 — but you're above the $500,000 phase-out threshold, so the exemption is reduced by 50% of ($750,000 - $500,000) = $125,000. Since that exceeds the $90,100 exemption, your exemption is zero.

AMT taxable amount: $750,000. AMT: $239,100 × 26% + $510,900 × 28% = $62,166 + $143,052 = $205,218. Tentative minimum tax: $205,218.

Since $205,218 exceeds your regular tax of $51,600, you owe AMT of $153,618 in addition to your regular tax.

That's $153,618 in tax on stock you haven't sold and may not be able to sell.

The AMT Credit: Getting Your Money Back (Eventually)

The AMT isn't a permanent tax — at least not in theory. When you pay AMT due to ISO exercises, you generate a minimum tax credit that carries forward to future years indefinitely. You claim it on IRS Form 8801.

Here's how it works:

In future years where your regular tax exceeds your tentative minimum tax (i.e., years where you wouldn't owe AMT), you can use the credit to reduce your regular tax bill. The credit can bring your tax down to — but not below — the tentative minimum tax for that year.

When do you typically recover the credit?

- When you sell the ISO shares (this usually generates enough regular tax to absorb the credit).

- When your income drops below the AMT threshold in subsequent years.

- Gradually over multiple years if neither of the above happens quickly.

The catch is that recovery can take years. In the meantime, you've paid real cash to the IRS on unrealized gains. If the stock price drops between exercise and sale, you may have paid AMT on gains that no longer exist — and your credit recovery timeline stretches even longer.

Five Strategies to Manage ISO AMT Exposure

1. Limit Your Annual Exercise Amount

The simplest strategy: don't exercise all your ISOs at once. Instead, calculate how many shares you can exercise each year without triggering AMT (or without triggering significant AMT).

The key number is your AMT exemption "crossover point" — the exercise spread that would push your AMTI above the level where AMT kicks in. For a single filer with $250,000 of regular income and the 2026 exemption of $90,100, you can tolerate roughly $340,000 of total AMTI before losing the full exemption. That means a spread of about $90,000 before you enter AMT territory (and much less before you lose the exemption entirely).

Spreading exercises over multiple years lets you stay in the exemption zone each year.

2. Same-Year Exercise and Sale (Disqualifying Disposition)

If you exercise ISOs and sell the shares in the same calendar year, the disposition is "disqualifying" — you lose the ISO's favorable capital gains treatment, and the spread is taxed as ordinary income on your W-2. But critically, there is no AMT adjustment because the income is already captured in the regular tax system.

This strategy makes sense when:

- The stock is publicly traded and you want to lock in gains.

- You're concerned about a stock price decline.

- The AMT cost of holding would exceed the benefit of long-term capital gains rates.

The trade-off: you pay ordinary income tax rates (up to 37% federal) rather than long-term capital gains rates (up to 20% federal). But you avoid the cash-flow nightmare of owing AMT on shares you can't sell.

3. Early Exercise + 83(b) Election

If your company allows early exercise — exercising options before they vest — you can exercise when the spread is small (or zero, at the time of your grant) and file an 83(b) election within 30 days. Because the spread at exercise is negligible, the AMT adjustment is negligible too.

All future appreciation becomes capital gains, not an AMT adjustment. This is the most powerful AMT-avoidance strategy available, but it requires:

- A company that permits early exercise.

- Cash to pay the exercise price.

- Willingness to risk losing money if you leave before vesting (you forfeit unvested shares but don't get your exercise price back).

4. Time Exercises Around the OBBBA Phase-Out Cliff

Under the new 2026 rules, the AMT exemption phases out at 50% per dollar above $500,000 (single). This means there's a sharp difference in AMT cost between staying below the phase-out threshold and being in the phase-out zone.

If your regular income is $400,000, you have about $100,000 of "room" before hitting the phase-out threshold. Exercising ISOs with a spread of $100,000 or less keeps you below the cliff. Exercising $300,000 of spread puts you squarely in the 42% effective marginal AMT zone.

Year-end planning is critical: if your income varies, exercise more in lower-income years and less in higher-income years.

5. Exercise Before Washington's Income Tax Takes Effect

This is the strategy nobody outside Washington is writing about.

Washington's 9.9% income tax takes effect January 1, 2028. For ISO holders, this creates a closing window of opportunity.

Currently, when you exercise ISOs in Washington, there is no state-level income tax on the exercise event. The AMT is a federal-only tax — Washington has no state AMT. So the only tax cost of an ISO exercise-and-hold is the federal AMT.

Starting in 2028, if your total income (including any ISO disqualifying disposition income or NSO spread) exceeds $1 million, Washington will impose 9.9% on the excess. This doesn't directly affect the AMT calculation — but it changes the calculus of the disqualifying disposition escape valve.

Here's why: if you exercise ISOs in 2028 or later and do a same-year sale (disqualifying disposition) to avoid AMT, the spread becomes ordinary income. If that pushes you past $1 million, you'll owe Washington 9.9% on the excess — a cost that wouldn't exist if you'd exercised in 2026 or 2027.

The planning window: Between now and December 31, 2027, Washington residents can exercise ISOs with no state income tax consequences whatsoever. After that date, the calculus changes permanently.

Washington State's Capital Gains Tax and Post-Exercise Shares

Once you've exercised ISOs and held the shares (paying the federal AMT), the next tax event occurs when you sell.

If you've met the ISO holding periods, the gain is long-term capital gains. At the federal level, that's 0%, 15%, or 20% depending on your income (plus the 3.8% net investment income tax for high earners).

In Washington, long-term capital gains above $250,000 are subject to the state's capital gains tax:

- 7% on gains between $250,000 and $1,000,000

- 9.9% on gains above $1,000,000

So the combined federal-plus-state rate on a large ISO qualifying disposition in Washington could be as high as 20% + 3.8% + 9.9% = 33.7%.

Compare that to a disqualifying disposition done before 2028 (where the spread is ordinary income with no state tax): 37% federal + 0% state = 37%.

The math gets interesting. For Washington residents exercising before 2028, the qualifying disposition (hold for capital gains) costs less than the disqualifying disposition (sell immediately for ordinary income) at the federal level, and neither triggers state tax. But you have to survive the AMT cash-flow hit in the interim.

The QSBS Wildcard

If your company is a C corporation with gross assets under $50 million at the time of your ISO exercise, the shares may qualify as qualified small business stock under Section 1202. If you hold the shares for at least five years, you can potentially exclude up to $10 million (or ten times your basis) in gain from federal tax entirely.

Under current Washington law, the QSBS exclusion also eliminates the state capital gains tax on the excluded gain.

This creates a scenario where:

- You exercise ISOs and pay AMT on the spread.

- You hold for five years (meeting both the ISO holding period and the QSBS holding period).

- You sell and exclude the gain from both federal and state tax.

- You recover the AMT credit against other tax liability.

If the QSBS exclusion applies, the AMT you paid at exercise is ultimately recoverable, and the total tax on potentially millions of dollars in gain could be close to zero. This is the best possible outcome for a Washington-based startup employee — but it requires everything to go right: the company must qualify, you must hold for five years, and the law must not change.

The Private Company Problem

All of these strategies assume some degree of liquidity. For employees at private companies, the AMT creates an especially painful problem: you owe cash tax on paper gains you can't monetize.

Some options if you're stuck:

- Partial exercises. Exercise only what you can afford to pay AMT on.

- Company-sponsored liquidity. Some companies offer tender offers or secondary sale windows. If yours does, time your exercises to coincide.

- Borrowing against shares. Some lenders will loan against private company stock. This is risky and expensive, but it exists.

- Negotiate extended post-termination exercise periods. If you're leaving the company, a standard 90-day exercise window forces a rushed decision. Some companies extend this to 5 or 10 years — ask.

The 2026 AMT Planning Checklist for Washington Residents

If you hold ISOs at a startup and live in Washington, here's what to do:

Now through December 31, 2027 (before WA income tax):

- Calculate your AMT crossover point. Use IRS Form 6251 or an AMT calculator to determine how much ISO spread you can absorb before triggering AMT. Factor in the new 2026 phase-out rules.

- Model a multi-year exercise plan. Spread ISO exercises across 2026 and 2027 to stay below the AMT phase-out threshold each year.

- Consider early exercise + 83(b). If your company allows it, this eliminates AMT risk on future appreciation.

- Check QSBS eligibility. Confirm the company is a C corporation with under $50 million in gross assets. If it qualifies, factor the five-year hold into your timeline.

- Exercise in a no-state-tax window. Every ISO exercise completed before January 1, 2028, avoids any Washington state income tax on the event — whether you hold or sell.

Starting January 1, 2028 (after WA income tax):

- Factor Washington's 9.9% into disqualifying disposition math. Same-year sales that generate ordinary income above $1 million will now cost an additional 9.9% at the state level.

- Revisit the hold vs. sell decision. The calculus shifts: holding for long-term capital gains (and paying the lower WA capital gains rate) becomes relatively more attractive compared to a disqualifying disposition (which now triggers WA income tax).

- Monitor the Washington QSBS landscape. There have been legislative attempts to subject QSBS gains to Washington's capital gains tax. If the law changes, the planning framework changes with it.

Key Takeaways

The AMT is the tax that punishes you for doing the thing ISOs are supposed to encourage — exercising early and holding for long-term gains. The 2026 OBBBA changes make it worse for higher-income filers by doubling the exemption phase-out rate.

For Washington residents, there's a specific planning window: between now and the end of 2027, ISO exercises incur no state-level tax of any kind. Once the income tax arrives in 2028, the math on every exercise decision changes.

The right strategy depends on your specific numbers — your income, your option spread, your company's QSBS eligibility, and your liquidity timeline. The framework above gives you the tools to run the analysis. But given the amounts involved, this is one area where working with a tax advisor who understands both the AMT and Washington's new tax structure is worth the investment.

Joe Wallin is a startup attorney at Carney Badley Spellman in Seattle. He advises founders, investors, and employees on equity compensation, QSBS, and Washington state tax planning. For more on equity compensation, visit the equity compensation resource page.

Related Reading

- Washington State Tax Planning Guide for High Earners

- Washington State Tax Calculator

- The Complete Guide to QSBS & Section 1202

- QSBS, Section 1202 & Section 1045

- Washington State Taxes