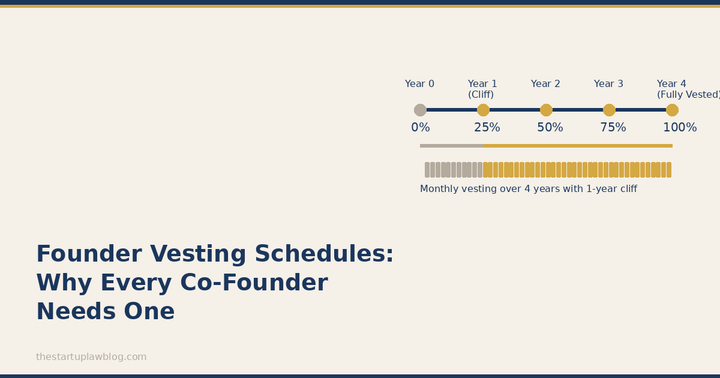

Equity Compensation Plan Design: How to Structure Your Startup's Stock Option Plan

Your equity compensation plan is one of the most important documents your startup will create. Here's how to structure it correctly — from pool sizing to vesting schedules to change of control provisions.