You sold QSBS stock in February 2026, expecting your $10 million gain to be fully sheltered by the federal Section 1202 exclusion — and your Oregon state tax bill to be $0. Here's why that expectation may be wrong.

Oregon has passed a significant tax conformity bill that directly affects founders, investors, and anyone relying on the federal QSBS exclusion.

Senate Bill 1507 changes how Oregon ties to the Internal Revenue Code by selectively decoupling from certain federal provisions — including the Section 1202 qualified small business stock (QSBS) exclusion.

The provision applies to sales of QSBS occurring on or after January 1, 2026.

⚠️ Important: As of April 4, 2026, Governor Kotek has not yet signed SB 1507 — but the bill becomes law automatically on approximately June 8, 2026 if no action is taken, and there is no indication of a veto. The provisions apply retroactively to tax years beginning on or after January 1, 2026.

The Key Change: Oregon No Longer Follows the Federal QSBS Exclusion

Oregon has historically conformed to federal taxable income with modifications. SB 1507 introduces targeted add-backs for items that are excluded at the federal level.

That includes:

- QSBS gain exclusion (Section 1202) — the entire framework, not just post-OBBBA changes

- 100% bonus depreciation

- Certain new federal deductions (e.g., auto loan interest)

The practical effect: income that is excluded from federal taxable income may still be taxed in Oregon.

What This Means for QSBS

Under federal law, qualifying QSBS gains can be excluded — often up to $15 million or 10x basis (and potentially higher for newer issuances under the One Big Beautiful Bill Act changes).

Under SB 1507:

- That excluded gain gets added back for Oregon tax purposes

- Oregon residents could face full state taxation on QSBS exits

- The add-back applies even to gain that would have been excluded if the stock had been sold before 2026

Example

A founder sells QSBS stock for a $10 million gain:

| Federal | Oregon | |

|---|---|---|

| Gain excluded | $10M | $0 |

| Tax owed on that gain | $0 | Up to ~$990,000 (at Oregon's ~9.9% top rate) |

This is a fundamental break from the federal framework.

A Critical Detail: It Only Applies to Oregon Residents

One of the most striking aspects of SB 1507 is that it applies only to Oregon residents. A nonresident selling the same QSBS — including someone who was a resident of Oregon shortly before the sale — would not be subject to this add-back.

This creates a significant planning dimension around domicile and residency timing relative to liquidity events.

For Oregon tax purposes, "resident" means someone domiciled in Oregon or someone who maintains a permanent place of abode there and spends more than 200 days in the state during the year. Domicile is your true, fixed, permanent home — the place you intend to return to. Simply spending time outside Oregon does not automatically change your domicile.

To successfully establish a new domicile before a liquidity event, you generally need to: (1) physically move to the new state, (2) take concrete steps to establish ties there (driver's license, voter registration, banking), and (3) clearly abandon your Oregon domicile. The timing and documentation of these steps matters significantly, and the window between a signed term sheet and closing can be very short. Anyone considering this path should work with a qualified multi-state tax advisor well in advance of any transaction.

Why Oregon Is Doing This

Oregon decoupled to protect its general fund — without SB 1507, the state would have automatically absorbed these federal changes at an estimated cost of $888 million over the 2025–27 budget cycle.

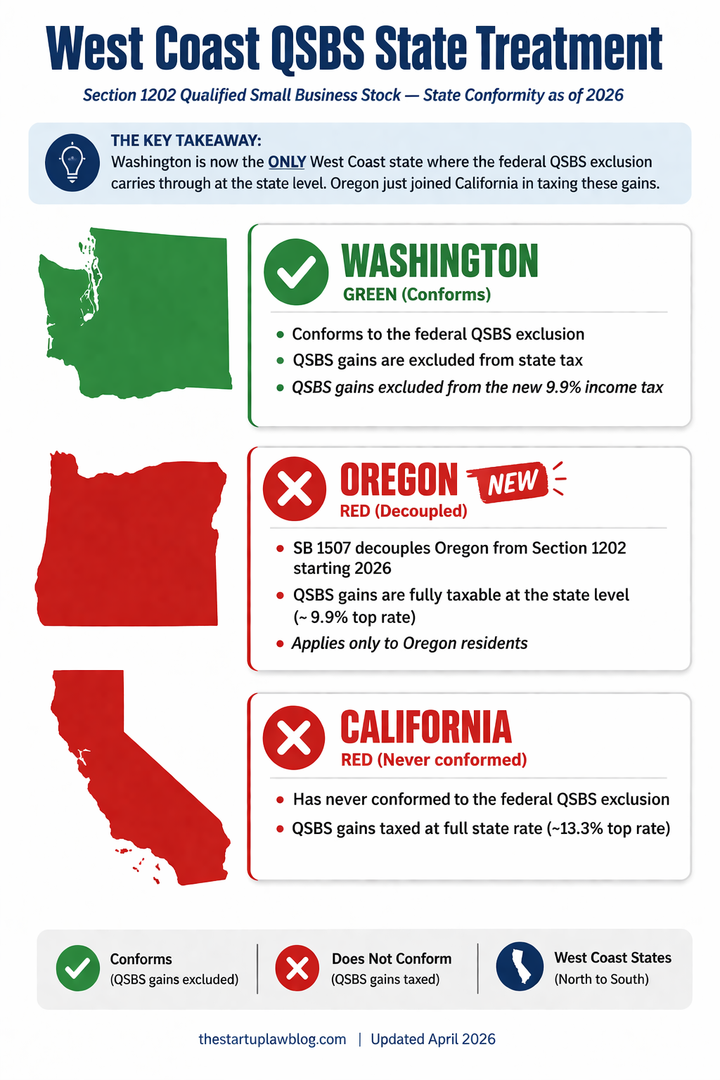

The West Coast QSBS Picture

Oregon's move puts the entire West Coast in an unfavorable position for QSBS holders:

- Washington — Conforms to the federal QSBS exclusion (QSBS gains are not subject to the new 9.9% income tax)

- Oregon — Decoupled starting 2026 (full state tax on excluded gains)

- California — Has never conformed to Section 1202 (QSBS gains taxed at the state level)

Washington is now the only West Coast state where the federal QSBS exclusion carries through to the state level.

For a full breakdown of how all 50 states treat QSBS gains, see our 2026 QSBS State-by-State Conformity Guide.

Status of the Bill

SB 1507 passed the Oregon House on February 25, 2026 on a 34–21 party-line vote. Governor Kotek has not yet signed the bill, but there is no indication of a veto. The bill becomes law automatically approximately June 8, 2026 (91 days after the session ends) if the governor takes no action.

The provisions apply retroactively to tax years beginning on or after January 1, 2026.

- January 1, 2026 — Effective date for the QSBS add-back (retroactive)

- February 25, 2026 — SB 1507 passed the Oregon House 34–21

- ~June 8, 2026 — Bill becomes law automatically if governor takes no action

Any QSBS sale occurring on or after January 1, 2026 by an Oregon resident may be subject to full state tax on the excluded gain.

Planning Considerations

For founders, investors, and advisors:

- Exit planning is now state-sensitive. Residency at the time of sale matters more than ever. Oregon residents approaching a liquidity event should evaluate whether a domicile change before the sale would be appropriate.

- QSBS no longer guarantees state-level tax efficiency. Federal exclusion ≠ state exclusion. This is now true across the entire West Coast except Washington.

- Geographic arbitrage is increasing. States that conform to federal QSBS treatment — including Washington, Texas, Florida, and others — become more attractive for founders planning exits.

- Timing decisions may shift. Founders who closed sales after January 1, 2026 while still Oregon residents may already be affected.

- Coordinate with multi-state tax advisors. Model the federal vs. state divergence before any significant transaction.

Frequently Asked Questions

Does SB 1507 affect QSBS sales that already closed in early 2026?

Yes. The provisions apply retroactively to tax years beginning on or after January 1, 2026. If you sold QSBS while an Oregon resident after January 1, 2026 — even before the bill was passed — you may owe Oregon state tax on gains that were excluded federally. Consult a tax advisor to understand your specific exposure.

What if I move out of Oregon before the QSBS sale closes?

If you successfully establish domicile in another state before the sale closes, the add-back should not apply — because SB 1507 only affects Oregon residents. However, this requires more than just physically leaving Oregon. You must clearly abandon your Oregon domicile and establish a new one. The timing, documentation, and intent all matter. See the residency section above for more detail, and work with a qualified tax advisor well in advance of any transaction.

Does this apply to all QSBS, or only stock issued after a certain date?

SB 1507 decouples Oregon from the entire Section 1202 framework — not just recent changes from the One Big Beautiful Bill Act. The add-back applies to any QSBS gain that would otherwise be excluded federally, regardless of when the stock was issued, as long as the sale occurs on or after January 1, 2026 while the seller is an Oregon resident.

What states still conform to the federal QSBS exclusion?

Many states — including Washington, Texas, and Florida — conform to the federal QSBS exclusion, meaning founders there owe no state tax on qualifying gains. California and Oregon do not. For a complete state-by-state breakdown, see our 2026 QSBS State-by-State Conformity Guide.

Bottom Line

Oregon SB 1507 materially changes the value of QSBS for state tax purposes.

QSBS remains powerful federally — but state-level outcomes are increasingly fragmented. For anyone planning a significant exit, ignoring state tax treatment is no longer viable.

For a complete breakdown of QSBS state conformity, see our 2026 QSBS State-by-State Conformity Guide.

For Washington-specific tax planning, see our Washington State Taxes hub and the Complete Guide to QSBS & Section 1202.

Have questions about how SB 1507 affects your specific situation? Contact us to discuss your QSBS planning needs.