If you earn over $1 million in Seattle, the 2028 tax picture splits in two: taxes you pay on your income, and taxes your employer pays for employing you. They get lumped into one alarming number, but only part of it actually leaves your paycheck. Here is who pays what.

The layers

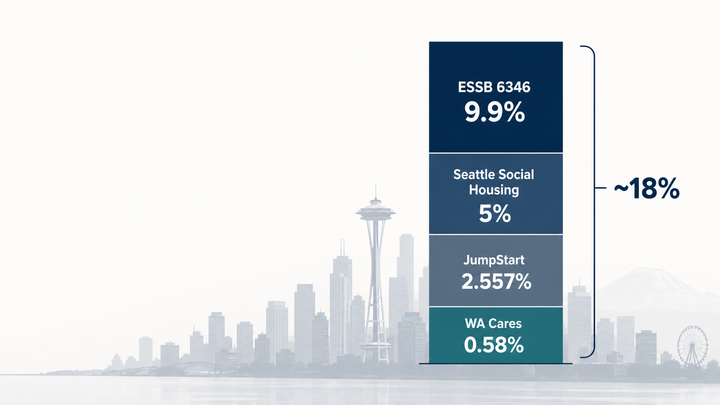

ESSB 6346 — 9.9%

Washington's new income tax takes effect January 1, 2028. It applies to household income above $1 million at a flat 9.9% rate. Wages, RSU vests, business income, partnership distributions — all of it. You pay this yourself.

Seattle Social Housing Tax — 5%

Approved by Seattle voters in February 2025 and in effect since January 1, 2025. A 5% tax on compensation above $1 million. RSUs count. Stock option gains do not. Critically, this is an employer tax that cannot be withheld from your paycheck — it is not part of your personal rate. If you own the company, your company bears it.

Seattle JumpStart Payroll Tax — up to 2.557%

In effect since 2021. Applies to compensation above applicable thresholds at companies with significant Seattle payroll, at a maximum 2026 rate of 2.557%. Like the Social Housing Tax, it is employer-paid and cannot be withheld from your wages.

WA Cares Fund — 0.58%

Washington's mandatory long-term care insurance payroll tax. Premiums have been collected since July 1, 2023. Applies statewide to all wage income. You pay it; your employer simply withholds it.

What you pay vs. what your employer pays

| Tax | Rate | Who pays |

|---|---|---|

| ESSB 6346 income tax | 9.9% | You |

| WA Cares Fund | 0.58% | You (withheld) |

| Your state & local total | ~10.5% | You |

| Seattle Social Housing Tax | 5.0% | Employer |

| Seattle JumpStart (max) | 2.557% | Employer |

| Employer payroll total | up to ~7.6% | Employer |

That's before a dollar of federal tax.

Add federal and the number gets uncomfortable

On wages, the top federal rate is 37%, plus the 0.9% Additional Medicare Tax on wages above $200,000 single / $250,000 joint. The 3.8% net investment income tax does not apply to wages — it applies to investment income.

Stack federal on top of the ~10.5% you pay at the state and local level, and your all-in marginal rate on wages above $1 million approaches 48% (37% + 0.9% + 9.9% + 0.58%). Your employer pays up to ~7.6% more in Social Housing and JumpStart tax on that same compensation — a real cost of creating a high-paying Seattle job, but not a deduction from your check.

The RSU problem

RSUs are particularly exposed. They vest as ordinary income, so you pay federal tax at ordinary rates plus ESSB 6346 and WA Cares — not capital-gains rates. They also count toward your employer's Social Housing and JumpStart base. A large RSU vest in 2028 can trigger all of these at once.

Stock option gains are carved out of both Seattle payroll taxes. But most tech workers receive RSUs, not options.

The planning window

WA Cares premiums began July 1, 2023, at 0.58% of wages. Statewide benefits become available July 1, 2026. So this is not new in 2028 — it is already in your paycheck.

If you're a Seattle-based founder or executive with significant income expected after 2027, the time to think about this is now — not after the exit.

Questions about your specific situation? Get in touch.