If you sold qualified small business stock and excluded the gain under IRC § 1202, you may be wondering whether Washington's new millionaire tax applies to that gain.

The short answer: it shouldn't.

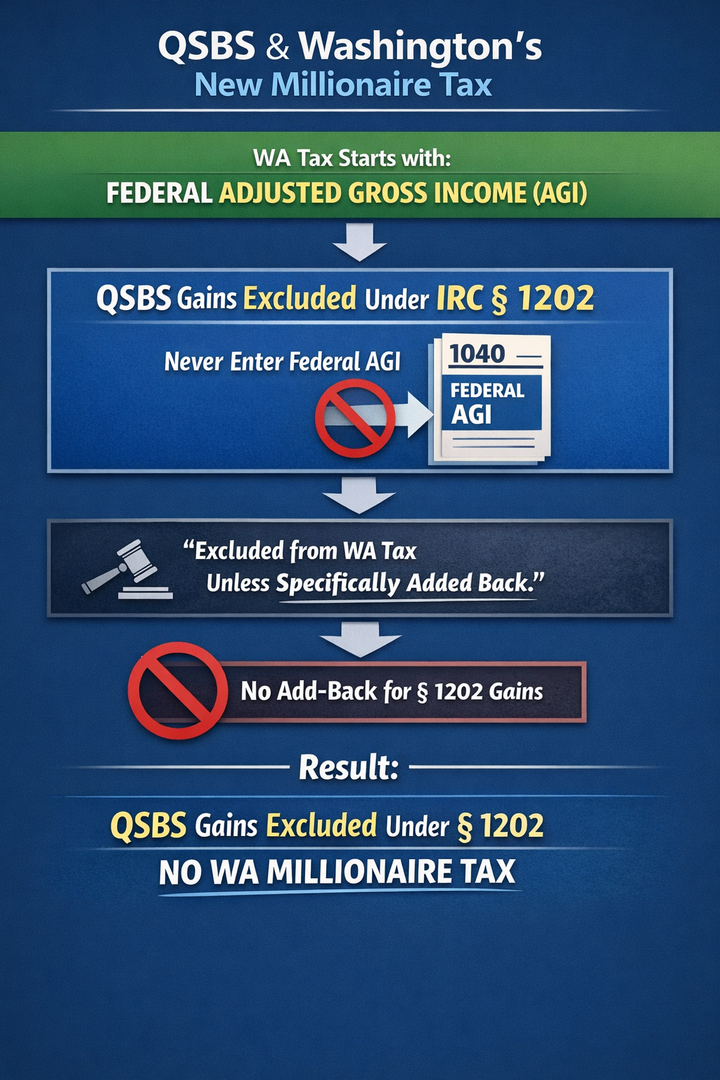

Washington's tax starts with your federal adjusted gross income (AGI). Gains excluded under § 1202 never enter your federal AGI in the first place — they're excluded at the federal level before AGI is calculated. Because the WA tax uses federal AGI as its starting point, and there is no specific add-back provision for § 1202 gains, those excluded gains should not be subject to the Washington millionaire tax.

For a deeper dive into how Washington's new income tax works — including the rates, thresholds, and what counts toward the tax base — read our comprehensive guide: Washington's New Income Tax: What Founders, Investors, and High Earners Need to Know.

This post is for informational purposes only and does not constitute legal or tax advice. Consult a qualified tax professional for advice specific to your situation.