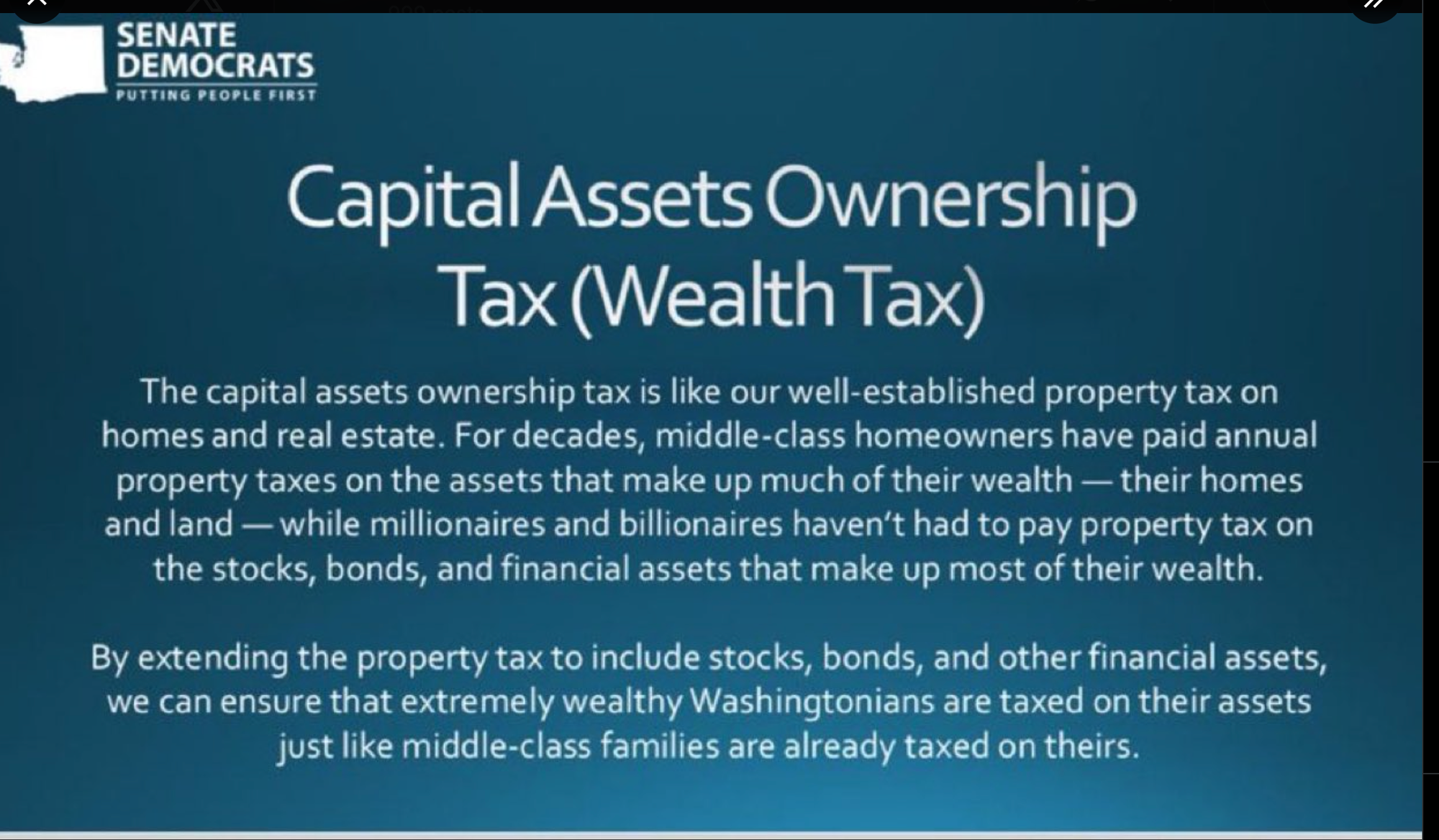

A blue graphic from Washington Senate Democrats has been making the rounds, promoting something called the "Capital Assets Ownership Tax" — pitched as extending the property tax to stocks, bonds, and financial assets held by the wealthy.

The graphic is real. The proposal it points to is real. It did not become law.

What did become law is something else, and the difference matters — both for what you should do right now and for what to watch next.

Source: Washington Senate Democrats, "2025 Revenue Discussion" (slide deck PDF, slide 15).

What the graphic actually refers to

The wealth tax push is split across two bills that have been live across the 2025-2026 biennium: SB 5797 in the Senate and HB 1319 in the House. Both would impose an annual tax on the value of intangible financial assets — stocks, bonds, ETFs, mutual funds — held above a threshold. SB 5797 set the threshold at $50M; HB 1319 set it at $100M. Both are framed exactly the way the graphic frames them: as "property tax fairness" applied to financial assets the way property tax already applies to your home.

Neither bill passed. As of the close of the 2026 short session, both remained in committee. Expect them to be reintroduced.

What did pass: ESSB 6346

Governor Ferguson signed ESSB 6346 on March 30, 2026. It imposes a flat 9.9% tax on Washington taxable income above $1 million per household, with federal AGI as the starting point. It takes effect January 1, 2028, and first returns are due in 2029. The Department of Revenue estimates roughly 21,000 filers in year one, with one-third concentrated in the 41st, 45th, and 48th legislative districts — Mercer Island, Bellevue, Medina, Hunts Point, Clyde Hill, Redmond, Issaquah, Sammamish.

This is a tax on income, not on net worth. A founder with $80M of private company stock and a $250K salary owes nothing under ESSB 6346 in any year they don't have a liquidity event. The tax is triggered by what you earn in a year — wages, RSU vesting income, bonuses, business income, partnership distributions, short-term gains, interest, dividends — not by what you own.

That's a different model from the wealth tax bills, and the distinction is the whole story.

The capital gains piece is already on the books

Worth flagging because most people miss it: Washington already has a 9.9% rate on long-term capital gains above $1M. That came in via SB 5813, signed in 2025. So if you sell concentrated stock today and the gain exceeds $1M above the standard deduction, you already pay 9.9% to Washington on the dollars above the cap. ESSB 6346 layers on top of that for non-capital-gain income — but provides a credit to prevent double taxation on the same gain.

The framing that "Washington has no income tax until 2028" stopped being accurate in 2025. The framing that "Washington just got a wealth tax" is also not accurate. The actual position is somewhere in between, and the line keeps moving.

Why these bills still matter

Seattle's PayUp law was a controlled experiment in what happens when you tax a behavior people can avoid by not engaging in it. The dynamic is broadly recognizable: tax design that ignores mobility produces less revenue than projected, and the cost lands somewhere unintended.

The wealth tax bills sit in the same category. The Department of Revenue's own fiscal analysis on HB 1319 estimates only 3,400 affected residents — a population small enough to relocate. France and most jurisdictions that tried broad wealth taxes walked them back for exactly this reason.

But the bigger point: the wealth tax frame is being normalized. When the legislature comes back, expect the threshold to move down, the rate to move up, or both — not because the policy works, but because the precedent of "we already tax some of this" makes the next step easier to argue for.

What to actually do right now

If you're in Washington and earning into the ESSB 6346 zone, the planning runway is the rest of 2026 and all of 2027. Specifically:

- Model your 2028 liability now, not in 2027. The decisions that matter — entity structure, domicile, exit timing, QSBS qualification — are slow to change and front-loaded in their effect.

- Confirm your QSBS status if you hold private company stock. Section 1202-excluded gains stay outside federal AGI, which means they stay outside ESSB 6346's base.

- Don't assume the wealth tax never comes back. If your plan depends on the threshold for taxing assets staying high, you don't have a plan.

The "Capital Assets Ownership Tax" graphic getting passed around isn't tomorrow's tax. ESSB 6346 is. Plan for what's law, but stay honest about the direction.

For the full mechanics of ESSB 6346 — including the marriage penalty, real estate carve-out, QSBS interaction, and constitutional challenge timeline — see Washington's New Income Tax: The Complete Guide for High Earners.