This article is for founders currently resident in Washington State who are hoping to transact this year (2026) or next year (2027) and want to lawfully minimize their exposure to Washington's capital gains tax, which is now tiered: 7% on the first $1 million of taxable gains, and 9.9% above that.

Before going down the residency path, run the QSBS analysis first. Washington's capital gains tax piggybacks on the federal Section 1202 exclusion, so gain that is excluded federally is generally excluded for Washington purposes as well. If QSBS fully covers your gain, you do not need to re-domicile. If QSBS covers only part of the gain, consider whether stacking the exclusion across non-grantor trusts can absorb the rest before turning to a move. Residency planning is the lever for the gain that QSBS and stacking cannot reach.

If you live in Washington and you are staring at a liquidity event, the state-tax exposure can become enormous very quickly. Washington's capital gains tax is tiered: 7% on the first $1 million of taxable gains (over the standard deduction) and 9.9% above that, so on a major founder liquidity event the state-tax bill can easily reach seven figures. The difference between being treated as a Washington resident and a nonresident at the time of sale can be enormous.

For Washington founders approaching a sale, residency planning has become one of the highest-stakes tax issues in the entire transaction.

The question I get more than any other right now is some version of:

"If I relocate to a state without an income tax — Nevada, Florida, Texas, Wyoming, Tennessee — before the deal closes, can I avoid Washington tax exposure on my gain?"

The honest answer is: sometimes yes. But Washington's residency rules are more detailed than most founders realize, and late-stage relocation planning can be harder than it appears. Below is how the rules actually work, the fact patterns that hold up, and the ones that don't.

Washington's Tiered Capital Gains Tax (7% / 9.9%)

Under RCW Chapter 82.87, Washington imposes a tiered excise tax on long-term capital gains above the standard deduction: 7% on the first $1 million of taxable Washington capital gains, and 9.9% on amounts above $1 million (verify the current DOR figure for the year of your sale). For a sale of stock or other intangible property, Washington generally taxes the gain only if the seller is domiciled in Washington at the time of sale. Tangible personal property follows separate allocation rules.

Two Pathways to Washington Residency

Washington's residency framework for the capital gains tax effectively has two separate pathways:

- Residency based on domicile, and

- Statutory residency based on maintaining a Washington place of abode and exceeding the Washington day-count threshold.

A founder can trigger one without triggering the other. Both have to be analyzed independently. Under RCW 82.87.020, you are a Washington resident for the capital gains tax if either:

- You are domiciled in Washington during any part of the year (with a narrow safe harbor if you maintain no permanent place of abode in Washington for the full year, maintain a permanent place of abode elsewhere for the full year, and spend 30 days or fewer in Washington), or

- You maintained a place of abode in Washington and were physically present in Washington for more than 183 days in the year.

Prong one is a fact-driven inquiry into where a person actually lives, intends to remain, and treats as their permanent home. Prong two is mathematical — a day count against a place of abode in Washington. A founder can fail either prong independently. The 183-day count, in particular, is a hard, objective number that is one of the first things the Department of Revenue examines.

Importantly, RCW 82.87.020 also recognizes part-year residency: a person is a resident only "for that portion of a taxable year" in which they were domiciled in Washington or maintained a place of abode here. That part-year language confirms that residency status can change during the year. But for stock and other intangibles, the operative allocation rule is RCW 82.87.100(b), which looks to domicile at the time of the sale — not just part-year status. That is the statutory hook that makes a genuine pre-closing change of domicile meaningful for a founder selling intangible property.

The Presumption of Continuing Domicile

Washington applies a rebuttable presumption that an established domicile continues until a new one is genuinely acquired. The Department of Revenue's rule states it directly: WAC 458-20-301 provides that "your domicile, once established, is presumed to continue," and that a Washington domiciliary bears the burden of proving the domicile changed. Washington case law goes back further: the Washington Supreme Court has long held that "the domicile, once established, continues until it is superseded by a new domicile," and that the burden of proof is on the person asserting the change. See Sasse v. Sasse; Fiske v. Fiske.

Two things follow.

First, intent alone is not enough. To establish a new domicile, you must be physically present at the new place and intend to make it your permanent home. The DOR rule expressly warns that selling the old home or acquiring a new one is "not conclusive." The Court of Appeals has framed the standard as "substantial evidence" of a real, present change — not future intent.

Second, in a sale-of-stock fact pattern, the timing question is whether the new domicile was established before the sale date. RCW 82.87.100(b) — the statute's core allocation rule for intangibles — allocates gain from intangible property by reference to the owner's domicile at the time of sale, and the Washington Supreme Court in Quinn v. State relied on Washington domicile as the constitutional nexus for taxing gains from the sale of intangibles. So if you start the year as a Washington domiciliary and sell mid-year, the burden is yours to show the move was real and complete by the closing date.

The statute itself does not create a conclusive whole-year rule. As noted, RCW 82.87.020 expressly contemplates part-year residency. That means a genuine mid-year change of domicile can take you out of Washington domiciliary residency from the date of the change forward — and gain on a post-move sale of intangibles — allocated under RCW 82.87.100(b) by domicile at the time of sale — can fall outside Washington's reach. But the presumption runs against you, the burden is yours, and the proof has to be objective and contemporaneous.

Where You Actually Sleep

Residency audits often become highly factual. Examiners may focus on where you actually slept at night, not merely where you worked during the day or maintained business interests. Calendars, cell tower data, credit card geography, and travel records all feed into that picture. If your nights are still in Seattle, the rest of the file is going to have to do a lot of work.

Domicile cases are ultimately about intent backed by objective facts. What you say privately matters far less than what your records, movements, and conduct show contemporaneously.

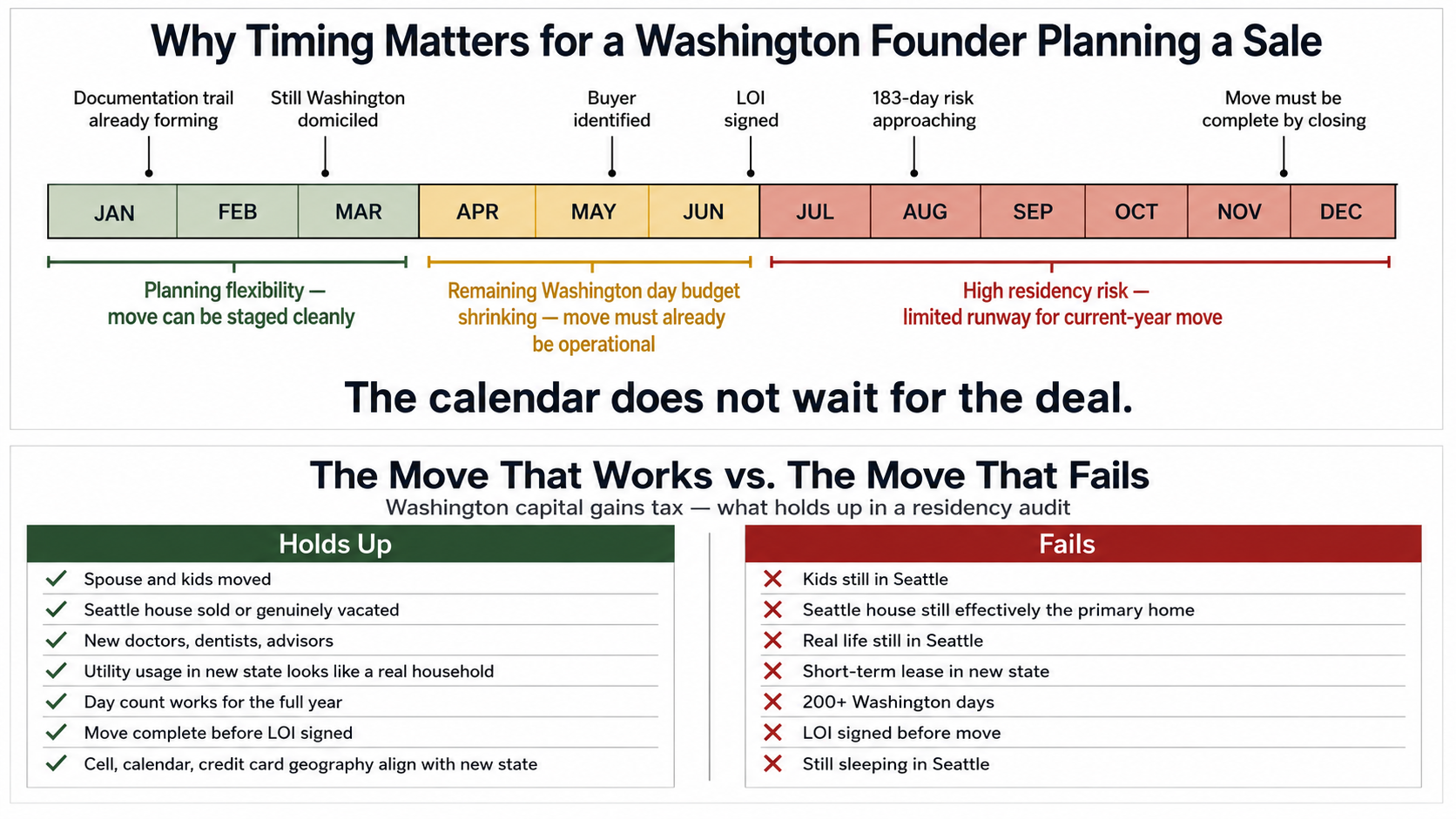

The Calendar Matters More Than Most Founders Realize — and It Is Already Running

For many founders, the real question is not whether they can move, but whether they can move early enough.

For founders already living in Seattle deep into the year, the planning window for the current tax year can narrow quickly. In practice, if a founder remains Washington-centered through the spring and summer, the remaining Washington day budget may become extremely tight, and in some cases the practical answer is that the move needs to happen immediately or the sale needs to move into the following year.

If it is already May or June and you have spent most of the year living in Seattle, the days you can safely spend in Washington for the rest of the year may already be limited. By late summer, some founders have effectively run out of runway for that tax year entirely, which can push the relocation strategy into the following year and complicate transaction timing.

This is one reason why residency planning often needs to begin well before a deal becomes imminent. The calendar does not wait for the LOI.

What Domicile Actually Means in Practice

For prong one, the DOR and courts look at the totality of the facts. WAC 458-20-301 provides a nonexclusive list of factors, including:

- Where your primary home is and where you actually sleep

- Where your spouse and minor children live

- Driver's license, voter registration, vehicle registration

- Bank and brokerage relationships

- Doctors, dentists, attorneys, accountants

- Office usage, executive role, board meeting locations, and where day-to-day management decisions occur

- Clubs, gyms, places of worship

- Where pets and other personal effects are kept

- Where your most valuable personal property is kept

- Federal and state tax mailing addresses

- Children's schools, professional licenses, in-state tuition, hunting and fishing licenses

- Where financial transactions originate

- Where you tell people you live

Business ties do not independently determine domicile, but they become evidentiary themes that examiners weave into a broader factual narrative. The DOR's rule treats this as a fact-intensive, totality-of-the-circumstances inquiry; no single factor is dispositive, and the rule expressly warns that selling the old home or acquiring a new one is "not conclusive."

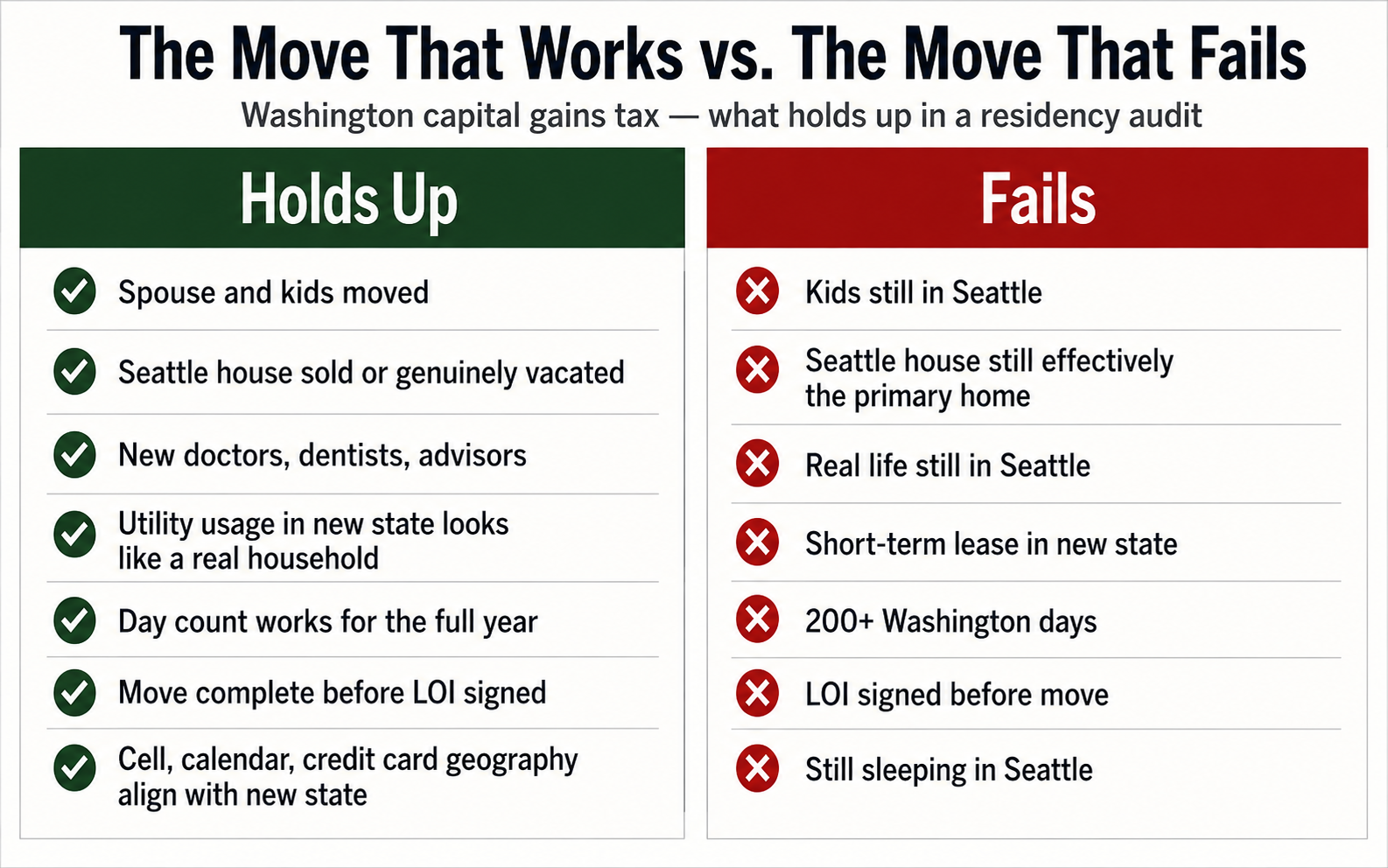

The Move That Works vs. The Move That Doesn't

In the deals I have worked on, the relocations that hold up have a consistent shape:

- Founder relocates before the LOI is signed — ideally well before the buyer is even identified

- Sells or genuinely vacates the Washington primary residence (or it becomes the kid's college house, the in-laws' place — and you can prove it)

- Buys or signs a real lease in the new state, moves furniture, ships the dog, switches doctors

- Spouse and minor children relocate

- The day-count math works for the full tax year of the sale

- Documentation is contemporaneous: utility bills, cell tower data, credit card geography, calendar entries, airline records

The most dangerous fact pattern is often the partial move — where the founder obtains a residence elsewhere but most family, social, and personal life remains centered in Washington. Apartment in Miami, spouse and kids still in Seattle, founder traveling constantly, Seattle house still effectively the primary home: that is the file that loses.

The more difficult cases usually involve late-stage moves where the underlying facts still point heavily toward Washington — for example, an LOI signed while the founder is still living in Seattle, a short-term out-of-state lease executed weeks before closing, more than 183 days spent in Washington during the year of sale, a spouse and children who never relocated, and contemporaneous records (board materials, calendars, credit card geography, social media) that continue to place the founder in Washington through and after closing.

The Department of Revenue does not need to reconstruct any of this. The records are already in writing. Do not manufacture evidence after the fact. Residency audits routinely examine records created contemporaneously in the ordinary course of life.

Earnouts, Rollover, and Installment Payments Make This Harder, Not Easier

If your consideration includes an earnout, rollover equity, installment payments, or post-closing consulting, the residency analysis does not end at closing — but the rules are different for each payment stream and should not be treated as a single bucket. Later-year domicile clearly matters for a later separate sale, including a future exit of rollover equity acquired at the original closing. Installment-sale gain from an earlier stock sale is recognized as payments are received under federal timing rules, but the allocation question still depends on domicile at the time the original sale occurred — not domicile when later payments come in. Earnouts require separate analysis depending on whether they are treated as additional deferred purchase price, compensation, or something else under the transaction documents and applicable federal tax characterization. The practical point remains: a clean residency position should be maintainable for every year in which transaction-related income is recognized, but the legal analysis for each stream is distinct.

This is a frequently overlooked issue. Relocation planning is often built around the closing date alone. The fuller picture requires analyzing each payment stream — closing proceeds, installment payments, rollover equity exits, and earnouts — under the applicable rules, which are not identical across stream types.

QSBS Generally Works in Washington

Because Washington starts from federal net long-term capital gain, gain excluded federally under IRC § 1202 is generally outside the Washington measure to that extent. That makes coordinated QSBS and residency planning especially valuable: a clean QSBS position can take a substantial portion of the gain off the table for federal and Washington purposes.

Filing Obligations

If Washington capital gains tax is owed, the taxpayer must file a Washington capital gains return by the federal due date, attach the federal return and supporting schedules, and generally file and pay electronically. If no tax is owed, a return generally is not required, although DOR's current web guidance says a return must still be filed if an extension was requested or a payment was made.

Timing Relative to Signing and Closing

By the time a buyer has been identified, NDAs are in place, and diligence is underway, the relevant facts are largely set. Examiners typically look at the 12 to 24 months around the closing date, and contemporaneous records — board materials, calendars, household activity — carry significant weight.

The strongest planning generally happens before the transaction is on the horizon. Waiting until after a binding transaction is effectively in place can materially weaken the planning position. For founders considering a sale within the next two years, residency analysis is most useful now.

What to Do Next: An Action Plan for a Washington-Domiciled Founder

You are domiciled in Washington today. You want to sell your business. Here is what the planning conversation looks like, in roughly the order it usually happens.

Step 1: Count your Washington days, today.

Before anything else, count the number of days you have already spent in Washington this year. Then count the days you realistically expect to spend here between now and December 31.

If you are maintaining a Washington place of abode and your Washington day count exceeds 183 for the year, the statutory-residency pathway is a major problem regardless of where you say you live. If your Washington day count exceeds 30 during the year, the narrow domiciliary safe harbor in the statute is unavailable. And if you started the year as a Washington domiciliary, the presumption of continuing domicile means the burden is on you to prove — by objective, contemporaneous evidence — that your domicile genuinely changed to another state before the sale.

A same-year sale is not impossible for a currently-domiciled founder. The statute recognizes part-year residency, and a real, completed move before closing can take post-move gain on intangibles out of Washington's domiciliary reach. But the presumption runs the other way, and the proof has to be solid. For most founders who have been living in Seattle through the spring, the cleaner path is to use this year to execute the move and target the sale for next year.

Step 2: Decide which year is your sale year.

Pick a target sale year and work backward from it. The year you close is the year that determines whether the gain is taxable in Washington. If you are still domiciled in Washington in your target sale year, every other piece of planning is downstream of that fact. The cleanest plans treat the move and the sale as belonging to different tax years.

Step 3: Pick the new state and commit to it.

Choose a new state of domicile and treat the move as a real life change, not a tax maneuver. Sign a long-term lease or buy a home. Move the family. Re-register vehicles. Change your driver's license, voter registration, and primary doctors. Update estate documents to the new state. The pattern that works is one where, looking back, your life clearly relocated.

Step 4: Time the move ahead of the deal, not alongside it.

Try to complete the move before a buyer is identified, before an LOI is signed, and before any binding deal terms are in place. For stock and other intangible property, the key allocation question is domicile at the time of sale — not whether the move predated the LOI. But a move completed well before the deal process is a stronger evidentiary pattern, because it is harder to characterize as driven by the transaction. A move executed alongside a pending closing will face greater scrutiny, even if the domicile facts are otherwise solid.

Step 5: Limit your Washington days after the move.

After the move, treat your Washington day count as a hard budget. Stay well under 183 for the year. A very narrow statutory carveout may apply if, for the full year, you maintain no Washington permanent place of abode, maintain a permanent place of abode elsewhere, and spend 30 days or fewer in Washington. Many founders will not satisfy all three requirements during a transition year. Note that spending more than 30 days in Washington does not by itself keep you domiciled in Washington — it only means the narrow full-year domiciliary safe harbor is unavailable. The core domicile question is still governed by the facts on the sale date. Track your days contemporaneously — do not reconstruct them later from memory.

Step 6: Address the Washington house and the Washington life.

If you keep the Seattle house, expect questions. The strongest fact patterns either sell the Washington home, lease it out at arm's length, or at a minimum genuinely vacate it as a residence. Holding a fully-furnished, ready-to-occupy Seattle home while claiming domicile elsewhere is one of the most common reasons residency positions fail. Changing the form of title to Washington real estate — for example, by transferring it into an LLC — may affect how a future transaction is characterized and whether certain exemptions apply, but it does not itself solve domicile. Washington treats individuals as beneficial owners of assets held through pass-through or disregarded entities for chapter 82.87 purposes. If you continue to use the Washington property as a personal home, retain easy occupancy, or leave family life centered there, the underlying domicile problem is factual, not a matter of how title is held. Any such restructuring has its own legal and tax implications and should be analyzed carefully with counsel before being implemented.

Step 7: Build the contemporaneous record.

Keep records as you go. Travel calendars, credit card statements, cell phone location data, utility bills, mail forwarding, lease or closing documents, and family-life records (school enrollment, doctors, gym memberships, club memberships) all matter. The goal is a paper trail that already exists by the time anyone asks for it. Do not manufacture evidence after the fact — build it in the ordinary course of life.

Residency audits routinely examine records created contemporaneously in the ordinary course of life.

Step 8: Coordinate residency with QSBS, rollover, and earnouts.

Once the residency picture is clear, layer in the deal-structure planning. Confirm QSBS qualification and the federal exclusion. Look at whether any portion of consideration is rollover equity, earnout, or installment payments, and analyze each stream separately. Later-year domicile clearly matters for a future exit of rollover equity. Installment gain from the original sale is recognized over time, but allocation turns on domicile at the date the original sale occurred. Earnouts require their own characterization analysis. A clean residency position should be maintainable for every year in which transaction-related income is recognized, but the analysis differs by payment type.

If you think a liquidity event may happen in the next one to two years, residency planning should probably start before the deal process formally begins. If you would like to discuss your specific situation, you can schedule a consultation here.

This post focuses on the residency and domicile framework that comes up most often in founder exit conversations. It is not a complete discussion of every issue that can arise in a Washington capital gains tax analysis. Asset-sale character and sourcing, Section 751 hot-asset components, compensation-versus-capital-gain earnout characterization, charitable planning, trust-based QSBS stacking, multi-state credits, and the 2025 and 2026 statutory amendments and broker-reporting changes all have their own complexities that require fact-specific analysis with counsel.

Joe Wallin is a Seattle-based startup and tax attorney. This post is general information, not legal or tax advice for your specific situation. Tax law changes; verify current figures and statutory text before relying on them.