QSBS and Washington's New Millionaire Tax: What Founders Need to Know

If you're a founder or early-stage investor in a Washington startup, you've likely heard the buzz about Washington's new income tax. In November 2023, the state passed ESSB 6346—a 9.9% tax on income above $1 million, scheduled to take effect on January 1, 2028. If you've also been fortunate enough to hold Qualifying Small Business Stock (QSBS) under Section 1202 of the tax code, you're probably wondering whether your gains will be subject to this tax when you eventually sell.

For the full analysis of ESSB 6346 — including the tax stack, marriage penalty, and residency rules — see Washington's New Income Tax: What Founders, Investors, Athletes, and High Earners Need to Know.

For the planning side — what to actually do before 2028 — see our Washington income tax action guide.

The short answer, for now, is no. Your federally excluded QSBS gains won't enter Washington's tax base in January 2028. But that's not the whole story—and the risk of future change makes this a critical planning issue for founders expecting a liquidity event.

This post is part of our Complete Guide to Washington's New Income Tax.

Understanding ESSB 6346: Washington's New Income Tax

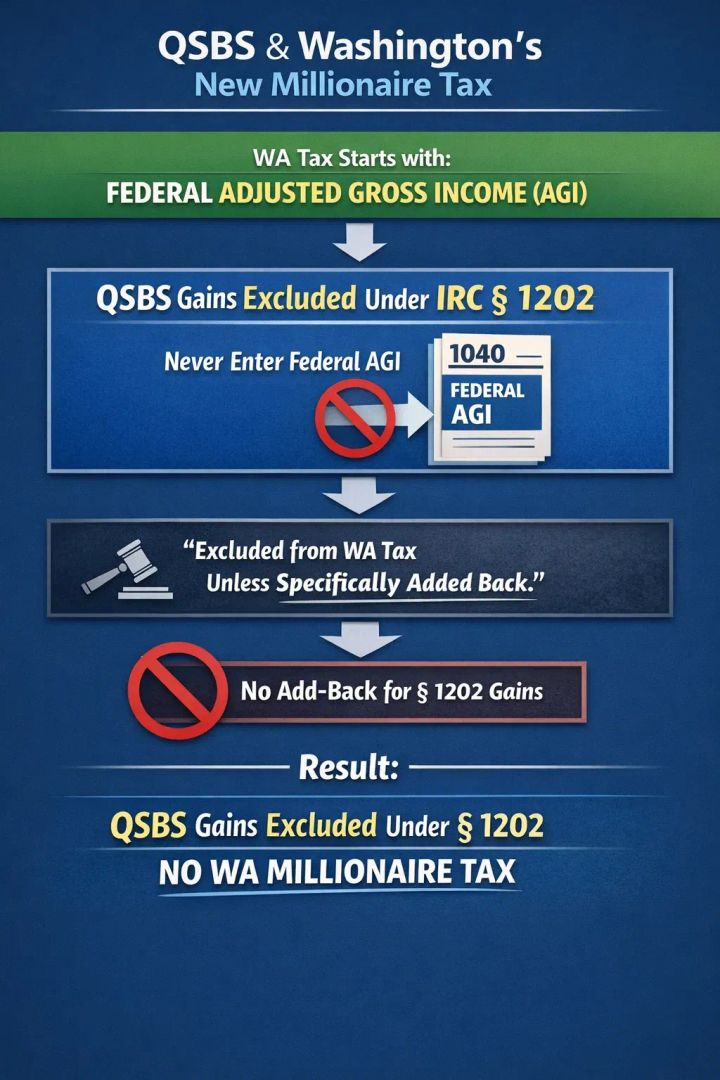

Let's start with the basics. Washington has historically had no state income tax—a significant advantage for high earners compared to California or New York. That changed with ESSB 6346, which imposes a 9.9% tax on the state's share of federal adjusted gross income (AGI) exceeding $1 million per individual (or $2 million for married couples filing jointly).

The law defines "Washington's share" as income earned by Washington residents or allocated to Washington under state apportionment rules. For most founders selling their company, this means Washington-source income from the sale will be included.

The effective date is January 1, 2028. If you're contemplating a liquidity event before that date, the gain entirely avoids Washington's new income tax. If you're timing a sale for after 2028, the income tax will apply—unless, of course, your gains are excluded from federal taxable income under Section 1202.

How Federal QSBS Exclusions Interact with Washington Taxation

Here's where QSBS becomes important. Section 1202 of the Internal Revenue Code allows shareholders to exclude 100% of the gain on qualified small business stock held for at least five years, up to a cap of $10 million per taxpayer per issuer (or ten times adjusted basis, whichever is greater). Note: the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, increased this cap to $15 million for stock acquired after enactment. Some of the highest-bracket shareholders can exclude up to 100% of their QSBS gains from federal income tax.

Washington's income tax is tied to federal AGI. AGI is calculated at the federal level and then applied to Washington's tax formula. When you exclude QSBS gains from federal taxable income, those gains don't appear on your federal return, so they don't enter Washington's AGI calculation either.

In practical terms: if you sell your QSBS for a $5 million gain and exclude all of it under Section 1202, your federal AGI remains unchanged (as if the sale never happened for income tax purposes). Since Washington's income tax is piggybacked on federal AGI, that $5 million exclusion means you're not subject to Washington's income tax on those gains.

So the current answer is straightforward. Federally excluded QSBS gains do not trigger Washington's new millionaire tax. You can sell, realize the gain, and keep the entire proceeds without the 9.9% state hit.

The Decoupling Risk: Learning from Oregon

But there's a caveat worth understanding, especially if you're planning around a longer timeline. While Washington currently conforms to federal QSBS exclusions, state legislatures can and do deviate from federal tax treatment.

Oregon offers the cautionary tale. In 2022, Oregon passed Senate Bill 1507, which decoupled from federal Section 1202 exclusions. Now, Oregon-source QSBS gains are fully taxable under Oregon's personal income tax, even though they're excluded federally. This means founders and investors with Oregon-source income on QSBS face a dramatic state-level tax that completely eliminates the federal benefit on their gains.

Could Washington do the same? Technically, yes. The legislature could amend the tax law to decouple and make QSBS gains taxable at the state level, even if they're excluded federally. Would they? That depends on future revenue needs, political will, and how the income tax revenue streams evolve. But it's a real risk—especially if Washington's income tax brings in less revenue than projected or if there's political appetite to broaden the tax base.

If you're holding QSBS and banking on a sale after 2028, you should be aware that a decoupling change is possible (if unlikely in the near term). It shouldn't necessarily change your strategy, but it should inform your risk assessment.

The Partial Exclusion Scenario: When Not All Gains Are Excluded

Not all QSBS qualifies for the full 100% exclusion. This is where things get complicated for founders and their advisors.

First, Section 1202 has an aggregate gains cap: the maximum excluded gain per taxpayer per issuer is $10 million (or ten times your adjusted basis, whichever is greater) for pre-OBBBA stock, and $15 million for stock acquired after July 4, 2025. If you and your co-founders invested $1 million and the company sells for $25 million, the total excluded gain is capped at $10 million, and the remaining $14 million is partially taxable.

Second, the exclusion percentage itself increases with holding period under the higher-bracket rule (applicable to 2010-and-later acquisitions under the "OBBBA" or Other Business Brought Back Act rules). If you hold QSBS for three years, you can exclude 50% of gains. At four years, it's 75%. Only at five years do you get the 100% exclusion.

Here's the crucial point: the portion of your QSBS gain that is not excluded under Section 1202 is included in your federal AGI. And if it's included in federal AGI, it flows through to Washington's income tax calculation.

Let me give you a concrete example. Suppose you hold QSBS from a company that qualifies for the OBBBA rules, and you sell it after holding for exactly four years. You have a $5 million gain. Under QSBS, 75% is excluded ($3.75 million), but 25% is taxable ($1.25 million). That $1.25 million enters your federal AGI and, therefore, your Washington taxable income. If you also have salary or other income that brings your total AGI over $1 million, the combination could trigger Washington's 9.9% tax.

This matters more than you might think. A $5 million partially-excluded QSBS gain combined with ordinary income could push a founder well over the $1 million AGI threshold, triggering the tax on the cumulative amount subject to tax.

The $1 Million Threshold and Cumulative Income Planning

Let's talk about the AGI floor itself. The 9.9% income tax applies to income above $1 million. If your federal AGI is $999,999, you owe no Washington state income tax. If it's $1,000,001, you owe 9.9% on the excess—in this case, about $10.

For high-earning founders, the threshold is often already exceeded from salary, dividends, capital gains on other investments, and so forth. But for bootstrapped founders who are income-light until their company exits, the threshold can be the difference between owing tax and owing nothing.

Here's where partial QSBS exclusions become relevant. If you have partially-taxable QSBS gains and you're planning your exit, the non-excluded portion could be the marginal dollars that push you over the $1 million line. Once you're over, the 9.9% applies to all income above that threshold—so the marginal dollars are actually very expensive.

Conversely, if you're below $1 million AGI, keeping your gain below the threshold through timing or structure could save significant taxes.

The Capital Gains Tax Interaction

Many founders also forget that Washington has an existing tiered capital gains tax (7% on the first $1M, 9.9% above $1M) on long-term capital gains from the sale of real property and certain business interests, effective since 2022. Unlike the new income tax, the capital gains tax applies regardless of AGI and regardless of whether gains are federally excluded.

So even if your QSBS gains are 100% federally excluded and avoid the new 9.9% income tax, they may still be subject to Washington's capital gains tax (9.9% on gains above $1M, 7% beneath, after a ~$270K standard deduction) if the stock sale meets the definition of a "long-term capital gain" under state law. This is another reason to carefully review the mechanics of your exit.

Exit Timing: Should You Sell Before 2028?

A common question I hear is: should we accelerate our exit to avoid the 2028 income tax?

If you have fully excluded QSBS and were otherwise planning to sell between 2028 and whenever, moving the sale before January 1, 2028, saves you 9.9% on your entire gain. That's not insignificant. On a $10 million gain, it's nearly $1 million in tax savings.

But several factors complicate this analysis. First, the company's value may grow over that time, making delay more profitable than acceleration. Second, if you haven't held your QSBS for five years yet, accelerating the sale means missing out on full Section 1202 exclusion—a federal tax that dwarfs the state tax. Third, bringing a deal to market takes time and depends on buyer appetite.

My general advice: don't let the 2028 date alone dictate your exit strategy. But if you're already considering a sale and timing is flexible, the January 1, 2028 trigger is worth marking on your calendar. If you can sell your fully-qualified QSBS by the end of 2027, you avoid $1 million in state tax. That's real money.

Planning Strategies for Founders Expecting a Liquidity Event

So what should you actually do? Here are some strategies I discuss with founders holding QSBS:

First, understand your QSBS position. Are the shares actually qualified small business stock under Section 1202? Have you held them long enough? This isn't always obvious. QSBS requires that the corporation be a C corporation (not an S corp or LLC), that it have less than $50 million in assets when you acquired the shares, and that substantially all assets be used in an active business. Many startups meet these requirements, but not all. If you're unsure, get clarification from your tax advisor.

Second, model the partial exclusion scenarios. If you don't yet have five years of holding, what's your actual excluded and taxable gain? If you'll have partially-taxable QSBS, how does it interact with other income? Run the numbers for holding an additional year to hit the next exclusion step (50% at three years, 75% at four years, 100% at five years). That year might mean the difference between owing Washington tax and avoiding it entirely.

Third, consider the 2028 date as a real inflection point. If you have fully-excluded QSBS and the business is saleable, January 1, 2028 is a meaningful deadline. Closing before that date avoids the 9.9% income tax. Closing after, you'll owe it (though this doesn't outweigh other factors like valuation or business timing).

Fourth, watch for decoupling risk. If you're contemplating a sale after 2030 or 2035, and Oregon's QSBS decoupling is a concern, stay informed about Washington legislative proposals. If a decoupling bill emerges, the calculus changes. For now, it's not an immediate risk, but it's worth monitoring.

Fifth, integrate your capital gains tax planning. Even if you avoid the income tax, you may owe Washington's capital gains tax (9.9% on gains above $1M, 7% beneath, after a ~$270K standard deduction). Work with your advisor to understand both exposures and whether any planning (like timing, entity structure, or buyer structure) can mitigate either tax.

What If Your QSBS Doesn't Fully Qualify?

Finally, let's address the scenario where your QSBS doesn't fully qualify—either because the company's assets exceeded $50 million when you invested, because the gain exceeds the $10 million cap, or because you haven't held long enough to hit the highest exclusion tier.

In these cases, your non-excluded gain is taxable at the federal level and will flow through to Washington's income tax. The calculation is straightforward: add the taxable portion of your QSBS gain to all other income, and if the total exceeds $1 million, the Washington 9.9% tax applies to the amount over the threshold.

The good news: if you're expecting a multi-million-dollar QSBS sale and you're already over the $1 million AGI threshold from other income, the marginal impact of additional taxable QSBS gain is "just" 9.9% (plus federal and capital gains taxes). The bad news: there's no planning around it. The tax applies. Your strategy should focus on maximizing the excluded portion (by hitting the five-year mark if possible) and understanding the true after-tax proceeds.

Bottom Line

Washington's new 9.9% income tax doesn't currently reach federally excluded QSBS gains. But your exit strategy shouldn't be built on that assumption alone. There are multiple moving parts: the five-year holding requirement, the partial exclusion scenarios, the $1 million AGI threshold, the existing 7% capital gains tax, and the risk of future decoupling.

If you're a founder or investor expecting a significant QSBS liquidity event, now is the time to map out your position with your tax advisor. Understand which gains are fully excluded, which are partially taxable, and how the timing of your sale interacts with both the 2028 effective date and your current AGI. That kind of planning can save you hundreds of thousands of dollars.

Questions about your own QSBS or Washington tax position? Let's talk. I help founders and investors navigate the intersection of federal and state tax planning, and QSBS is one of my favorite topics to dig into.

Keep Reading

- Does QSBS Avoid Washington’s New 9.9% Income Tax? (Yes — For Now)

- Washington's New Income Tax: The Complete Guide for Founders, Investors, and High Earners

- stock option Exercise Timing: Planning Before Washington's 2028 Income Tax

- ING Trusts Won't Save You from Washington's Income Tax. Here's What Might.